USA Rare Earth released the latest USAR Earnings Reports for Q1 FY2026 after the market closed on May 13. Specifically, USA Rare Earth (Nasdaq: USAR) delivered a double beat: revenue came in at $5.7M (vs. $4.2M consensus, a 35% beat) and adjusted EPS landed at −$0.12 (vs. −$0.14 consensus, a $0.02 beat). While the GAAP net loss reached $67.0M, the company’s cash reserves climbed to a massive $1.75 billion following the $1.5B PIPE financing that closed in January. Consequently, shares fluctuated in extended trading—initially popping 1–3% before settling around −0.86% at $25.33. We provide the full breakdown in the “What Actually Happened” section below.

The Setup: Why USAR Earnings Reports Are Now Policy Reports

USA Rare Earth, Inc. (Nasdaq: USAR) reports its first-quarter fiscal 2026 results after market close on Wednesday, May 13, 2026. Therefore, the print serves as the first earnings release since the company became — both literally and financially — a Trump administration policy vehicle.

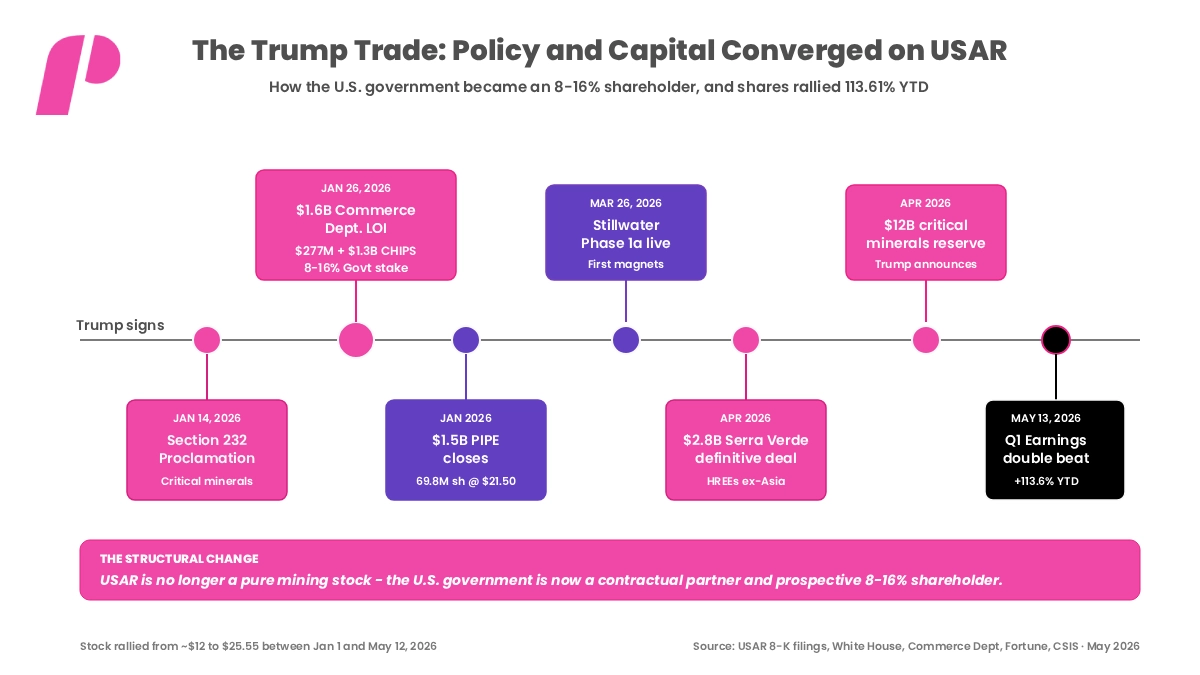

On January 26, 2026, the U.S. Department of Commerce announced a non-binding $1.6 billion funding package for USAR. This includes $277 million in direct federal funding plus a $1.3 billion senior secured loan through the CHIPS Act, exchanged for 16.1 million shares of common stock and 17.6 million warrants. Depending on warrant exercise, the U.S. government will own between 8% and 16% of the company. Furthermore, no precedent exists in recent decades for the federal government taking a direct equity position of this size in a publicly traded mining and manufacturing company.

Two days earlier, on January 14–15, 2026, President Trump signed a Section 232 proclamation. This directive mandates trade negotiations on processed critical minerals and their derivative products. Importantly, the proclamation explicitly reserves the right to impose tariffs or set minimum import prices if negotiations fail to address “national security risks.” Six weeks later, the administration announced a $12 billion critical minerals stockpile program. Consequently, USAR sits at the intersection of every single one of these initiatives.

For traders running a trading program around policy-driven names, this matters because the equity story no longer relies on pure mining economics. Instead, it focuses on how aggressively the U.S. government underwrites the build-out of a domestic rare earth supply chain, and how quickly USAR can convert that policy support into operating revenue. As a result, shares have surged 113.61% year-to-date heading into the print, closing at $25.55 on May 12 against a $5.54 billion market cap. Meanwhile, the options market priced an expected post-earnings move of ±9.42%.

Background: What Are Rare Earths, and Why Does Trump Care?

Before diving into USAR Earnings Reports, investors must understand what the company actually mines and manufactures. Accordingly, this is the kind of context that turns stocks for beginners from speculative coin flips into informed positions.

Rare earth elements (REEs) comprise 17 chemically similar metals — including neodymium, praseodymium, dysprosium, terbium, samarium, and yttrium. These metals act as essential inputs into permanent magnets, semiconductors, defense systems, electric vehicle motors, wind turbines, and AI data center cooling infrastructure. Geologically speaking, they are not actually “rare.” However, companies find them extremely difficult and environmentally costly to separate and process.

The strategic problem revolves around concentration. For instance, China currently produces about 70% of the world’s rare earth elements and controls roughly 80–90% of global processing capacity. Furthermore, the United States currently possesses zero operational heavy rare earth separation capacity. In April 2025, China imposed export licensing requirements on multiple rare earths and derivative magnets, which triggered a months-long disruption for U.S. automakers, defense contractors, and electronics manufacturers. By June 2025, the Trump administration negotiated a partial restoration of access, but the chokehold remains the central vulnerability in U.S. industrial policy.

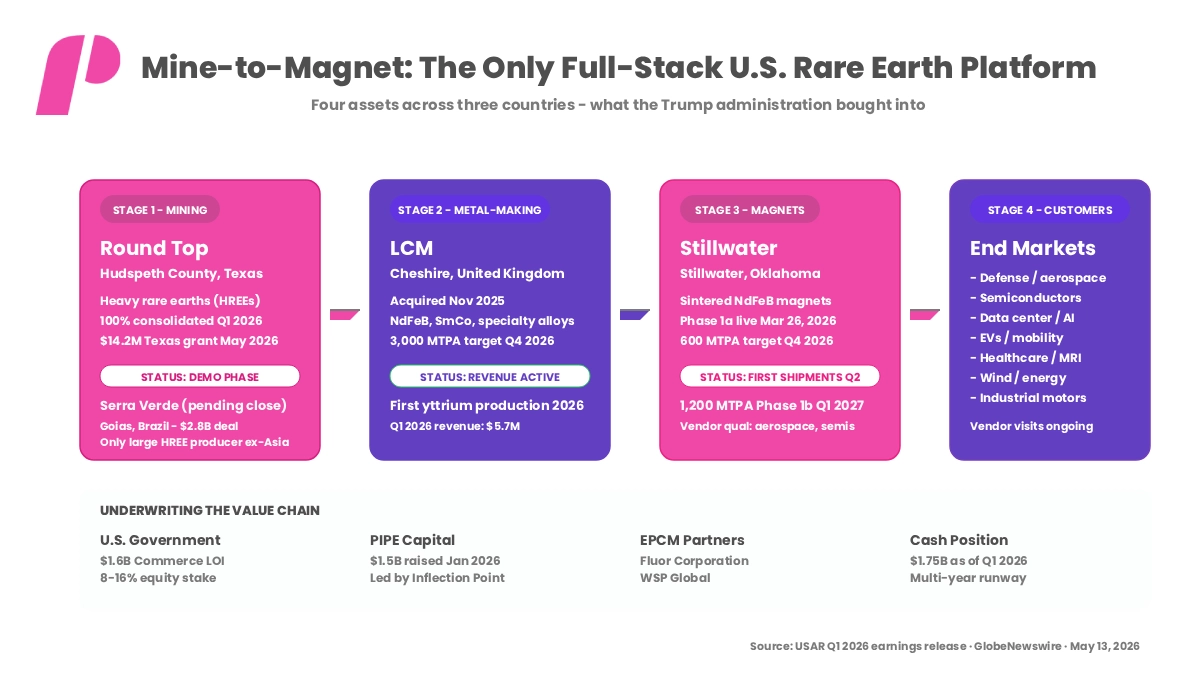

Consequently, USAR responds to this vulnerability with what the company calls a “mine-to-magnet” platform. The company controls every step from extraction (Round Top, Texas) through processing and metal-making (LCM in Cheshire, UK; planned Colorado hydrometallurgical demonstration) to neodymium magnet manufacturing (Stillwater, Oklahoma). Moreover, they now incorporate mining capacity outside Asia (Serra Verde in Brazil, pending close). Because no other U.S.-domiciled company has assembled this complete vertical integration, the federal government chose USAR.

The Headline Numbers and What’s Expected

Because USAR remains in the early commercial phase — barely revenue-generating in Q4 FY2025 — the cleanest framing pairs the prior quarter’s actuals with the Q1 FY2026 consensus.

Financial Performance: Q4 FY2025 Actuals vs. Q1 FY2026 Consensus

| Metric | Q4 FY2025 Actual | Q1 FY2026 Consensus | Read |

|---|---|---|---|

| Revenue | $1.64M (Inaugural Revenue) |

$4.20M | LCM ramping |

| Adjusted EPS | −$0.19 | −$0.14 to −$0.22 | Wide consensus range |

| Net Loss (GAAP) | $50.2M | ~$60M expected | Higher stock-based comp |

| Cash & Equivalents | $359.9M | ~$1.75B post-PIPE | $1.5B PIPE closed Jan |

| Magnet Production | Pre-commissioning | Phase 1a active | First shipments Q2 |

| Government Funding | LOI signed Jan 26 | Definitive May target | Closing risk |

Analyzing the Structural Takeaways

Ultimately, USAR Earning Reports do not yet focus on reading the income statement. Instead, they highlight cash adequacy (now extraordinary at $1.75B), execution against operational milestones (Stillwater Phase 1a, LCM expansion, Round Top consolidation), and the conversion of the U.S. government LOI into a definitive funding agreement, which management targets for sometime in May 2026.

USAR Earnings Reports: Reading the Pre-Print Scorecard

Three numbers describe USAR heading into the May 13 print: revenue, cash, and the status of government deals.

The Q4 FY2025 print told investors what to expect: lumpy, ramping, very early commercial revenue from the Less Common Metals (LCM) UK acquisition that closed in November 2025. Specifically, LCM currently produces the dollars on USAR’s income statement. The facility sells rare earth metals and alloys (including the first commercial yttrium production achieved in Q1 2026) to industrial customers in defense, aerospace, and industrial motor markets.

Then, in January 2026, the company fundamentally changed its entire equity story. The $1.5B PIPE closed at $21.50 per share (69.8 million shares issued), the Commerce Department announced the LOI, and shares began an unbroken rally that has now compounded to +113.61% YTD. Subsequently, three strategic announcements layered onto that base: a definitive $2.8B agreement to acquire Serra Verde Group (the only large-scale heavy rare earth producer outside Asia, located in Goiás, Brazil), 100% economic consolidation of the Round Top project in Texas, and a $14.2 million Texas Semiconductor Innovation Fund grant.

Revenue Composition: LCM Today, Magnets Tomorrow, Mining the Year After

USAR generates revenue across four eventual streams, and each carries very different unit economics. However, today, only one of them produces dollars on the income statement.

Revenue Strategy: Streams, Recognition Timeline, and FY2026 Operational Catalysts

| Revenue Stream | Recognition | First Material Revenue | FY2026 Catalysts |

|---|---|---|---|

| Metal & Alloy Sales (LCM, UK) | On delivery | Active (Q4 2025+) | 3,000 MTPA target by Q4 2026 |

| Magnet Sales (Stillwater, OK) | On delivery | Q2 2026 (first shipments) | 600 MTPA by Q4 2026 |

| Rare Earth Oxide Sales (Round Top, TX) | On delivery | 2028+ | Hydrometallurgical demo Q2 2026 |

| HREE Concentrate (Serra Verde, Brazil) | On delivery | Post-close (Q3 2026) | $2.8B acquisition pending |

The Structural Importance of Magnet Economics

What makes the Stillwater magnet ramp structurally important is the underlying unit economics. Specifically, sintered neodymium-iron-boron (NdFeB) magnets and samarium-cobalt (SmCo) specialty magnets command premium pricing when operators domesticate and qualify them for defense applications. Management commissioned Phase 1a on March 26, 2026, and they guided the first commercial shipments to begin in Q2 2026. Furthermore, management targets 600 MTPA of run-rate magnet capacity by Q4 2026 and 1,200 MTPA by Q1 2027 (Phase 1b). Beyond that, vendor qualification visits from semiconductor, industrial motor, heavy equipment, and aerospace customers occurred consistently throughout Q1.

The Trump Trade: How USAR Became the Policy Vehicle

The single most important relationship in any review of USAR Earning Reports involves the company’s relationship with the Trump administration. Indeed, this dimension makes USAR fundamentally different from MP Materials (NYSE: MP), Energy Fuels (NYSE: UUUU), or any other rare earth peer in the U.S. equity market. Three policy actions established the framework.

First, the January 14, 2026, Section 232 proclamation directed the Commerce Department and U.S. Trade Representative to negotiate agreements. The proclamation notably reserves the right to impose tariffs or minimum import prices if negotiations fail. Second, the January 26, 2026, Commerce Department LOI provided USAR with a $1.6 billion funding pathway — $277M in direct federal funding plus a $1.3B CHIPS Act loan — in exchange for an 8% to 16% federal equity stake (subject to warrant exercise). Third, the April 2026 announcement of a $12 billion U.S. critical minerals stockpile program created a potential buyer of last resort for domestic rare earth production.

Trading Implications of a Hybrid Private-Public Entity

Consequently, what this means for traders: USAR now operates as a hybrid private-public company. The U.S. government maintains a structural economic interest in the success of USAR’s mine-to-magnet platform. Therefore, Phase 1a Stillwater commissioning acts as a national security milestone. Serra Verde’s closing represents a foreign-policy event. Moreover, defense industrial strategy documents now report magnet shipment cadence.

However, the downside of becoming a policy vehicle is the dilution math. The combined effect of the $1.5B PIPE and the Commerce Department equity package implies roughly 50%+ shareholder dilution from the January 2026 baseline. Existing holders share the upside with the federal government and institutional PIPE investors. Thus, for traders evaluating this name — especially in a trading program that scales position size based on conviction — modeling the fully diluted share count is non-negotiable.

Wall Street’s Verdict

Analyst coverage on USAR is concentrated but unusually bullish. The most recent average price target sits at roughly $34–37 across covering firms, against the $25.55 pre-print close. The dispersion is narrower than what you typically see in pre-commercial stocks — a function of the policy floor created by the government deal.

Analyst Outlook: Institutional Ratings and Price Targets

| Firm | Rating | Target | Core View |

|---|---|---|---|

| Benchmark | Buy | $45 | Highest target; capacity doubling thesis |

| Cantor Fitzgerald | Buy | $35 | Government LOI validates roadmap |

| Roth/MKM | Buy | $35 | Funding accelerates the timeline |

| Canaccord Genuity | Buy | $33 | Lower WACC on financing certainty |

| William Blair | Buy | n/a | “Assumption of more govt funding to come” |

| Consensus (~5–6 analysts) | Strong Buy | ~$34–37 | 5 Buy / 1 Hold / 0 Sell |

The bull case anchors on the government partnership as a floor under valuation, the magnet capacity ramp as the near-term revenue catalyst, the Serra Verde acquisition as a global market repositioning event, and the broader policy tailwind from Section 232 measures, the $12B stockpile program, and ongoing China decoupling. The bear case is straightforward: a sub-revenue company at a $5.5B+ market cap, with 50%+ dilution already in the share count and additional government warrants outstanding, requires the magnet ramp and Serra Verde closing both to execute on schedule to justify current pricing.

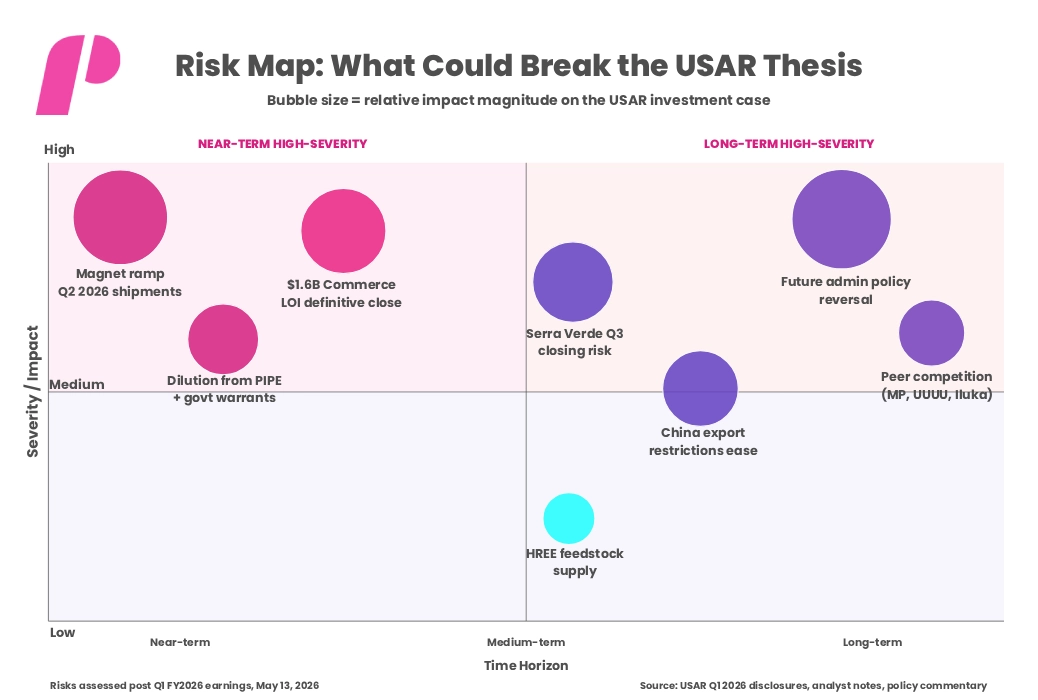

What USAR Earnings Reports Reveal About the Risks Ahead

Policy-driven small-cap industrial names are among the highest-variance investment categories in public markets. Within that category, USAR sits at the high-narrative, high-execution end. Any reading of USAR Earning Reports should be done against a risk picture that includes policy, dilution, execution, and competitive dimensions.

Near term, the magnet shipment cadence out of Stillwater Phase 1a is the cleanest tiebreaker for the bull thesis. Fulfillment is guided to begin in Q2 2026, but the first commercial deliveries have not yet been reported. Any quarter where Stillwater slips — particularly if vendor qualification visits from aerospace and semiconductor customers fail to convert into purchase orders — will pressure the stock disproportionately because so much of the current valuation is forward-looking.

Medium-Term Policy Execution Risks

Medium term, the definitive U.S. government funding agreement remains the central policy-execution risk. The April 2026 target slipped; consequently, management now expects definitive documentation in May 2026. Each subsequent slip raises the question of whether the LOI converts into committed dollars or evaporates as a non-binding letter. Similarly, the same logic applies to the Serra Verde acquisition, with a Q3 2026 closing target pending stockholder approval.

Long-Term Existential and Competitive Risks

Long-term, existential risks include policy reversal and Chinese policy normalization. For example, the Trump administration has already walked back portions of earlier rare earth signaling. Furthermore, a future administration could simply not exercise the warrants, decline to enforce Section 232 trade remedies, or roll back the critical minerals stockpile.

Separately, if China meaningfully eases its rare earth export restrictions, the price premium that supports USAR’s thesis compresses. Competition is also rising from MP Materials, Energy Fuels, and Iluka Resources. This is not a “stocks for beginners” position without first understanding the dilution math and the policy-driven valuation. Ultimately, the same volatility that produced the 113% YTD rally can

USAR Earnings Reports: What Actually Happened – The May 13 Print

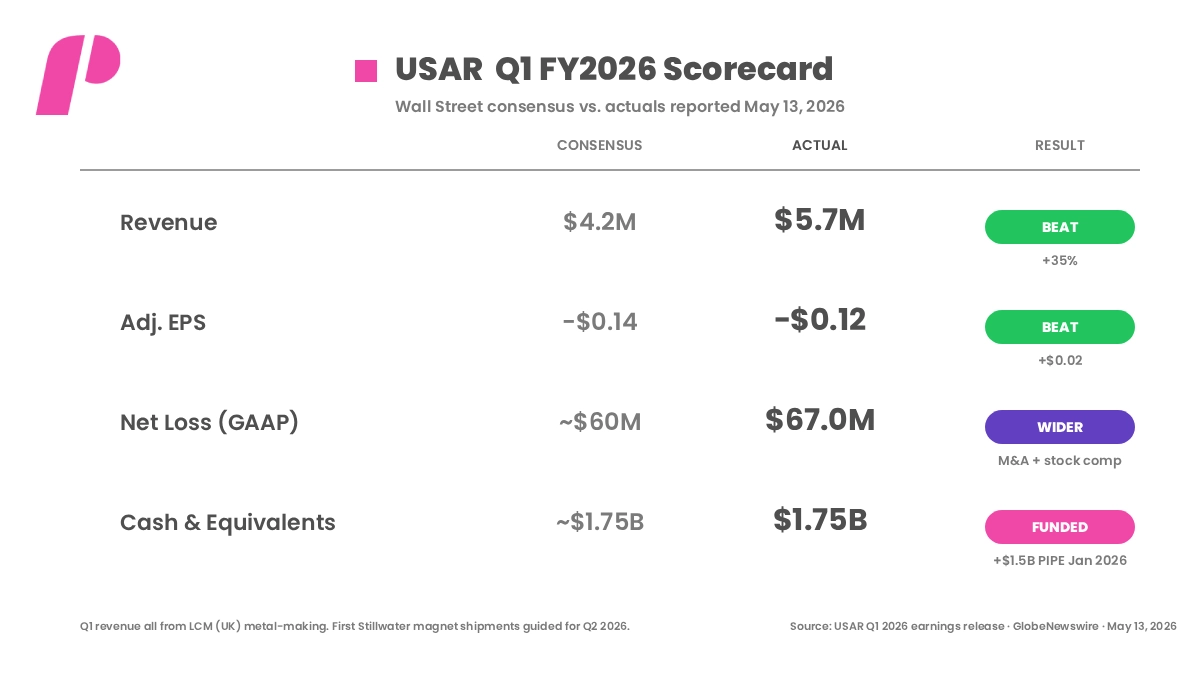

USA Rare Earth released Q1 FY2026 results after market close on May 13, 2026, followed by a 5:00 p.m. ET earnings call hosted by CEO Barbara Humpton and CFO Rob Steele. The headline result was a clean double beat — better than the consensus on revenue and on EPS — with the bigger story being the layering of strategic transactions across the quarter.

The reported scorecard

- Revenue: $5.7M — beat the $4.2M FactSet/Quiver consensus by 35%. All Q1 revenue derived from LCM metal-making operations in Cheshire, UK; gross profit was a slim $0.1M (1.9% gross margin) with management guiding for margin expansion as LCM utilization rises through 2026.

- Adjusted EPS: −$0.12 — beat the consensus range of −$0.14 to −$0.22 (the wide spread reflects how few analysts cover the name with consistent methodology); $0.02 beat against the central −$0.14 estimate, or a 14.29% positive surprise.

- GAAP loss per share: −$0.34 on $67.0M net loss attributable to USAR — a meaningful step-up from $50.2M in Q4 2025, reflecting M&A-related expenses and stock-based compensation. Ongoing operating expenses, excluding those items were approximately $25M.

- Adjusted net loss: $24.1M vs. $12.0M in Q1 2025 — a ~100% widening that reflects the expense ramp ahead of meaningful magnet revenue.

- Cash & marketable securities: $1.75 billion — versus $359.9M at year-end FY2025, a ~$1.4B increase driven by the $1.5B PIPE that closed in January.

- Operating cash use: $18.6M vs. $10.3M in Q1 2025; loss from operations $36.7M vs. $8.7M.

The strategic actions were the real news

Q1 was less about earnings and more about reshaping the company’s commercial footprint:

- $1.5B PIPE financing closed January 2026 — 69.8M shares issued at $21.50, led by Inflection Point with major mutual fund participation. The capital raise is what makes the cash position what it is.

- $2.8B Serra Verde acquisition definitive agreement — announced April 2026, targeted to close Q3 2026, subject to stockholder approval. Serra Verde owns the Pela Ema mine and processing plant in Goiás, Brazil — the only large-scale producer of heavy rare earth elements (HREEs) outside Asia. The deal includes a 15-year 100% offtake agreement with price floors.

- 100% economic consolidation of Round Top — the heavy rare earth project in Hudspeth County, Texas, previously held through Texas Mineral Resources.

- Phase 1a Stillwater commissioned March 26, 2026 — first commercial NdFeB magnet shipments guided for Q2 2026. Targeting 600 MTPA capacity by Q4 2026.

- LCM Cheshire UK expansion announced — metal and alloy capacity expanding to 3,000 MTPA by Q4 2026, driven by demand for SmCo, NdFeB, and specialty alloys.

- $14.2M Texas Semiconductor Innovation Fund grant — announced May 12, 2026, to accelerate Round Top Mountain.

- Fluor + WSP Global selected as EPCM partners — engineering, procurement, and construction management for the accelerated mining plan at Round Top.

Stock reaction: muted

Shares moved within a tight range in extended trading on May 13: initially up roughly 1.5% (Benzinga reported $25.80 in after-hours), then drifting to −0.86% at $25.33 by the close of the extended session per Investing.com data. The reaction reflects two competing reads: (1) the operational and financial results clearly beat expectations, but (2) the magnet shipment cadence and the definitive U.S. government funding agreement remain unresolved, and the options market had priced an outcome roughly two times more volatile than the print delivered.

What the print confirmed about the preview thesis

The central preview claim — that USAR Earnings Reports are now policy reports as much as financial reports — was confirmed. Management’s prepared remarks framed the company explicitly as “the partner of choice for the advanced materials that underpin Western national security and technological innovation.” The Q1 financial details mattered, but the milestones that moved the equity story were the PIPE close, the Serra Verde definitive agreement, and the still-pending U.S. government definitive funding agreement targeted for May 2026.

What is yet unresolved is the definitive U.S. government funding agreement timing. Management reiterated a May 2026 target but did not provide a specific date. The next material catalysts to watch in Q2 are: (1) first magnet shipments from Stillwater, (2) execution of the definitive Commerce Department funding award, and (3) stockholder vote progress on the Serra Verde acquisition.

USAR Earnings Reports: The Bigger Picture

USA Rare Earth has now printed its first earnings report as a hybrid private-public industrial company. The post-mortem confirms what the preview anticipated: this is not a quarter to be measured purely by revenue or EPS. It is a quarter that codified a $1.6B government funding pathway, deployed $1.5B in PIPE capital, committed $2.8B to acquire the only large heavy rare earth producer outside Asia, and started commercial magnet operations at Stillwater for the first time in U.S. history at this scale.

Beyond this print, the next 12 months will tell the longer story. The definitive U.S. government funding agreement closing — now targeted for May 2026 — is the immediate regulatory milestone. The Q2 Stillwater magnet shipment ramp is the immediate operational milestone. The Q3 Serra Verde closing is the immediate strategic milestone. The June 3, 2026, annual meeting and a forthcoming Investor Day are the immediate communication milestones.

Assessing the Long-Term Investment Thesis

Whether USAR remains a sustainable investment at $25 depends on whether the Trump administration’s rare earth policy compounds into operating revenue and recurring contracts on a 2026–2030 timeframe. For instance, Bank of America and similar consultancies frame the global rare earth reshoring opportunity as a multi-hundred-billion-dollar capital cycle through 2035. If those projections hold true, USAR’s integration positions it as the most-leveraged single name to that thesis in the U.S. equity market.

Conversely, if the policy tailwind ebbs — through a U.S.-China rapprochement, a future administration’s reversal, or simple execution slippage — the stock will be revalued against a much smaller domestic addressable market. Ultimately, USA Rare Earth executed the financing, the M&A, and the regulatory positioning. However, it has not yet converted those moves into recurring magnet revenue.

Final Takeaways for Traders

The lone takeaway from this round of USAR Earnings Reports: USA Rare Earth has completed the foundational work. For retail traders working through a structured trading program, the lesson dictates that USAR is not a stock you trade on the earnings number alone. Instead, you trade it on the milestones that the earnings report happens to disclose along the way. Therefore, this distinction makes USAR Earning Reports worth reading carefully, not skimming.

Disclaimer: This article is for informational/educational purposes only and is not financial advice or a guarantee of results. Trade The Pool uses simulated funds for evaluation; becoming a funded trader depends on performance and is not guaranteed. Trading involves risk of loss, and past performance does not indicate future results. Services may be restricted in certain jurisdictions. Always conduct independent research and consult a professional before trading.

If you liked this post make sure to share it!