Oklo Inc. (NYSE: OKLO) reports its first-quarter fiscal 2026 results via its OKLO Earnings Reports on May 12 after market close. Furthermore, the print is the first checkpoint after a 30% rally driven by two specific catalysts: U.S. Nuclear Regulatory Commission (NRC) approval of the Aurora powerhouse Principal Design Criteria (PDC) topical report on May 6, and a strategic partnership with Nvidia and Los Alamos National Laboratory on AI-enabled reactor research.

Consequently, the setup is unusual. Oklo has no operating reactors, no revenue, and consensus is for an EPS loss of $0.19 against zero revenue. Specifically, Wall Street’s price target ranges from $60 (UBS) to $150 (Texas Capital), a 2.5x spread that captures how differently analysts model a pre-revenue advanced fission company with a 14 GW customer pipeline and $2.54B in liquidity.

Moreover, shares closed at $78.13 ahead of the print, up roughly 30% over the prior month and 177% off the 52-week low of $28.16, but still 60% below the 52-week high of $193.84. Ultimately, this is what trading a pre-commercial regulated industrial company looks like: range, not direction.

Therefore, the metrics that matter for OKLO Earnings Reports are different from those of a traditional income-statement company. Additionally, cash runway, milestone progress on the Aurora-INL combined license application (COLA), and the conversion path from non-binding letters of intent to binding power purchase agreements will determine whether the stock

The Headline Numbers and What’s Expected in OKLO Earnings Reports

First, because Oklo is pre-revenue, the cleanest framing pairs the Q4 FY2025 actuals with the Q1 FY2026 consensus setup and overlays the cash position, which is the operative balance-sheet metric.

Financial Performance: Q4 FY2025 Actuals vs. Q1 FY2026 Consensus

| Metric | Q4 FY2025 Actual | Q1 FY2026 Consensus | Read |

|---|---|---|---|

| Revenue | $0 | $0 | Pre-revenue, by design |

| EPS (Non-GAAP) | −$0.27 | −$0.19 | Missed by 59% in Q4 |

| Net Loss | $39M+ | ~$30M | Headcount + stock comp ramp |

| Cash & Marketable Securities | ~$1.4B | $2.5B+ expected | Post-ATM raise |

| Customer Pipeline | ~14 GW | ~14 GW | Held steady |

| Aurora-INL Target First Ops | Late 2027 | Late 2027 | Timeline intact |

Notably, the cash-burn question is the most important relationship in any review of OKLO Earnings Reports. Oklo entered 2025 with roughly $1.4 billion in cash. Furthermore, a 2025 at-the-market (ATM) equity program completed in Q1 2026 issued about 12.4 million shares for net proceeds of approximately $1.18 billion. Consequently, the combined effect: Oklo now has one of the deepest cash positions among pre-commercial advanced-reactor developers, but it has also undergone dilution to get there.

Reading the Pre-Print Scorecard for OKLO Earnings Reports

Thus, three numbers describe Oklo heading into the May 12 print: the cash position, the consensus EPS loss, and the customer pipeline.

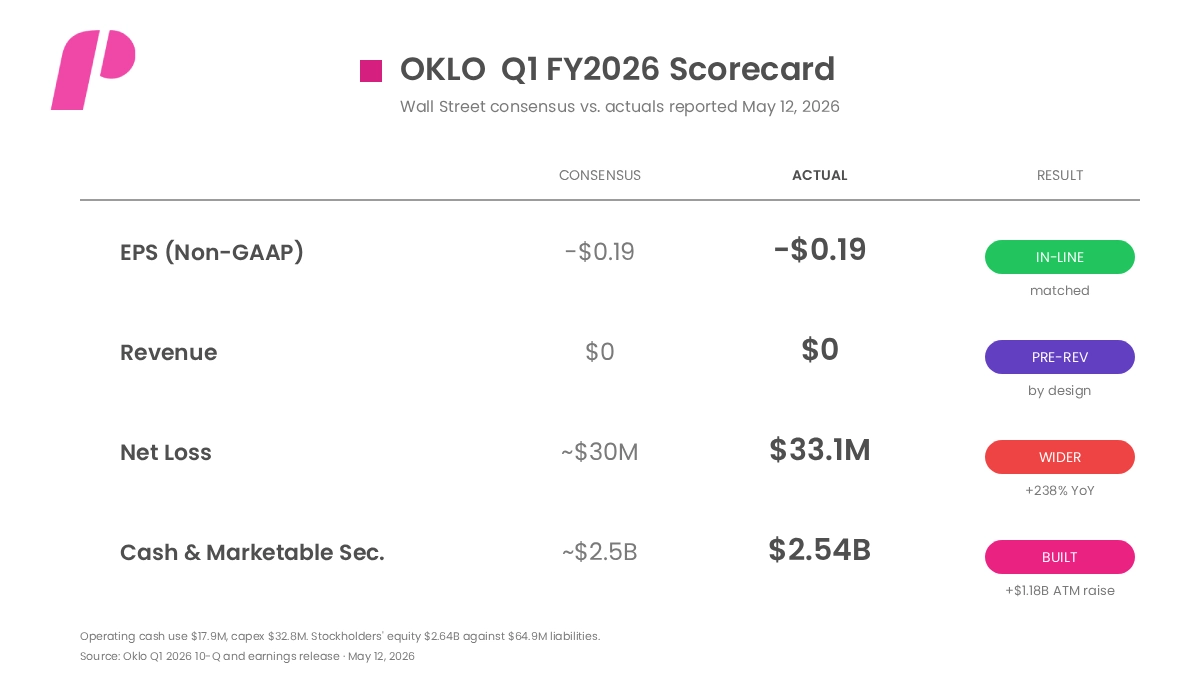

Consensus vs. Actual Q1 FY2026 Scorecard

Indeed, the Q4 FY2025 print told investors what to expect. EPS came in at −$0.27 against a −$0.17 consensus, a 59% miss. However, the miss wasn’t operationally meaningful (R&D and G&A timing), but it did signal that Oklo’s expense ramp is accelerating ahead of any revenue inflection. Therefore, Q1 FY2026 consensus assumes that the ramp continues at scale.

Subsequently, in April 2026, the catalyst stack delivered exactly as promised. On May 6, the NRC approved the Aurora PDC topical report on an accelerated review schedule less than half the traditional timeline. Importantly, the PDC establishes the foundational safety and design framework that every future Aurora license will reference. Moreover, in the same window, Oklo announced its Strategic Partnership Project with Battelle Energy Alliance and its Nvidia/Los Alamos AI-reactor design collaboration. As a result, the rally to $78 followed.

Ultimately, the structural takeaway: Oklo’s value breaks down into three buckets: regulatory progress, customer conversion, and cash adequacy. Consequently, Q1 OKLO Earnings Reports address all three, but not in the income statement format most investors are used to reading.

Revenue Composition: There Isn’t One Yet in the OKLO Earnings Reports

First, Oklo will have four eventual revenue streams once Aurora goes commercial. However, none of them produced dollars in Q1 FY2026. Importantly, the unit economics matter because they define what an income statement looks like once the first reactor energizes.

Revenue Strategy: Streams, Recognition Timeline, and FY2026 Catalysts

| Revenue Stream | Recognition | First Recognition Year | FY2026 Catalysts |

|---|---|---|---|

| Power Purchase Agreements (PPAs) | Ratable over contract | 2027 (Aurora-INL) | COLA Phase 1 filing |

| Fuel Recycling (HALEU) | On delivery | 2028+ | DOE fuel award |

| Heat Sales (industrial) | On delivery | 2028+ | Diamondback Permian site |

| Government Contracts | Milestone | 2026 (NNSA, DOE) | Genesis Mission alignment |

| Total FY2025 Revenue | — | $0 | Pre-commercial |

Furthermore, what makes the Aurora business model structurally interesting is the build-own-operate framework. Unlike traditional reactor vendors who sell hardware and recognize lumpy revenue, Oklo plans to own the reactors and sell the electricity, a model closer to an independent power producer (IPP) than a manufacturer. Consequently, once Aurora-INL energizes in late 2027 (target), revenue should be a long-duration recurring stream priced under PPAs with names like Switch, Meta, and Equinix.

The Customer Pipeline in OKLO Earnings Reports: 14 Gigawatts of Letters of Intent

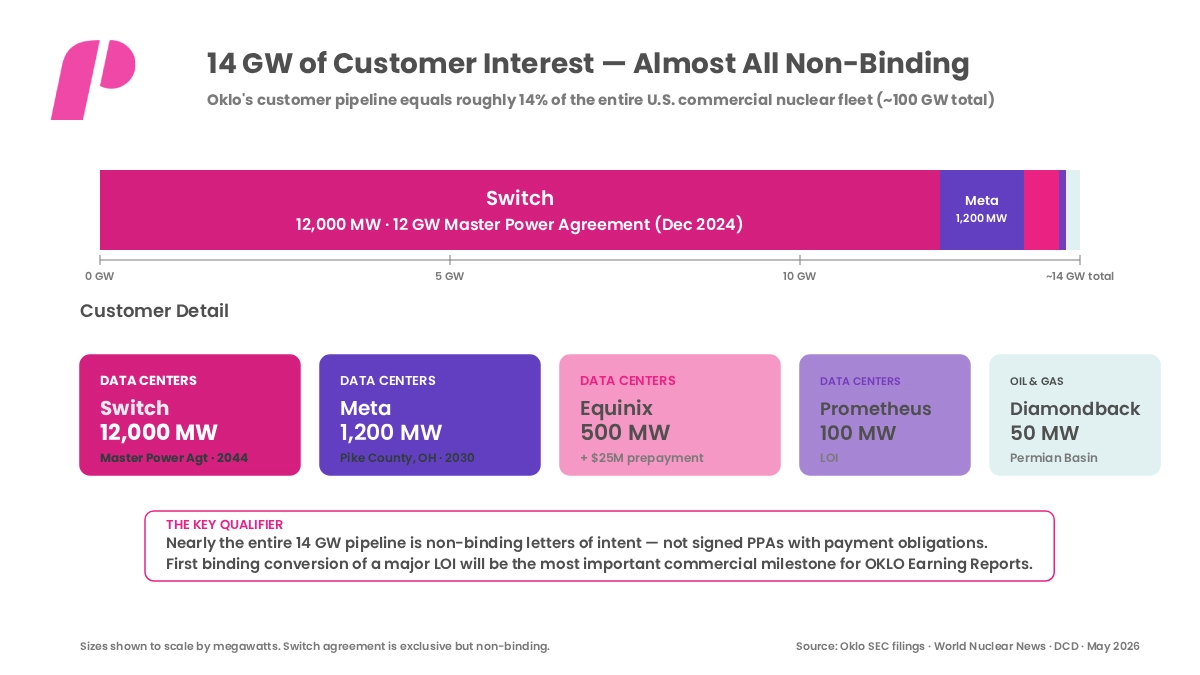

Undoubtedly, the single most important chart in any review of OKLO Earnings Reports is the customer pipeline. Specifically, Oklo has roughly 14 GW of customer interest, equivalent to about 14% of the entire current U.S. commercial nuclear fleet. Importantly, the qualifier matters: nearly all of this is non-binding.

Oklo Customer Pipeline Breakdown — 14 GW Across Data Centers, Energy, and Government

Specifically, the pipeline anchors on a single transformative agreement: a 12 GW non-binding Master Power Agreement with Switch, signed in December 2024, to deploy Aurora powerhouses across the U.S. through 2044. Additionally, that single agreement represents more capacity than every other quoted Oklo customer combined. Moreover, layered on top: Meta’s 1.2 GW Ohio campus agreement, Equinix’s 500 MW pre-agreement with $25M prepayment, Prometheus Hyperscale’s 100 MW letter of intent, and Diamondback Energy’s 50 MW for the Permian Basin.

Ultimately, this is the proof window. Consequently, OKLO Earnings Reports are supposed to clarify over the next 12 to 18 months. Investors want to see at least one letter of intent. Typically, the smaller, earlier-stage ones convert into a binding power purchase agreement with payment obligations. However, Q1’s print did not deliver that conversion, but it also wasn’t expected to.

The Strategic Pivot: Becoming the AI Power Default

Subsequently, in late April 2026, Oklo formalized two relationships that crystallize the strategic narrative around the company’s positioning. Specifically, the Nvidia and Los Alamos National Laboratory partnership applies AI methods to advanced reactor and fuel-system design via the Prometheus AI platform and Oklo’s Multiphysics infrastructure. Combined with the customer pipeline, this is the most consequential narrative shift in Oklo’s commercial story.

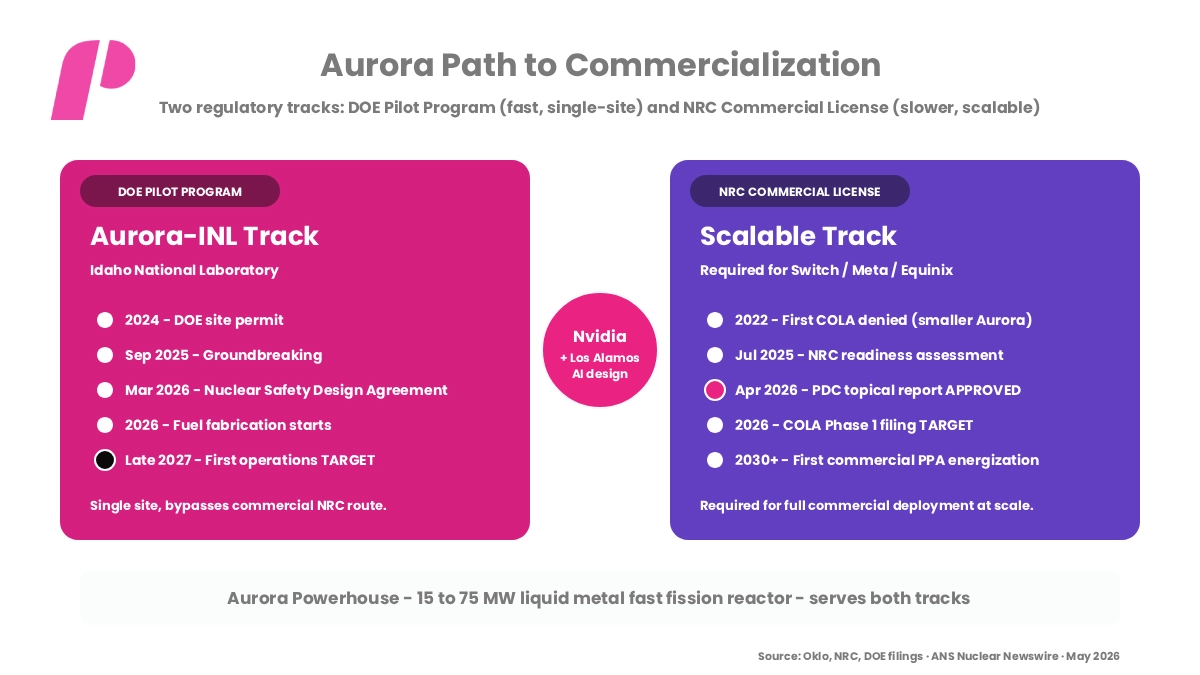

Aurora Path to Commercialization: DOE Pilot Track + NRC Commercial Track

Specifically, the two regulatory tracks solve different problems. Furthermore, the DOE Reactor Pilot Program, under which Oklo is deploying Aurora-INL, bypasses the traditional commercial NRC licensing route and targets first operations by late 2027. Moreover, the Idaho Operations Office approved the Nuclear Safety Design Agreement for Aurora at INL in March 2026. This is the fastest path to a powered, operating reactor; however, it is single-site and not replicable for commercial customers.

In contrast, the NRC commercial track is what Switch, Meta, Equinix, and every other commercial customer requires. Furthermore, the April 2026 PDC approval is the foundational document for that track, establishing the safety and design framework that every future Aurora license will reference. Additionally, Oklo targets filing Phase 1 of the Aurora-INL combined license application (COLA) in 2026.

Therefore, the investment thesis embedded in the dual-track strategy is clear: AI data center buyers eventually need exactly what Oklo designs to deliver: reliable, carbon-free, behind-the-meter baseload power. Ultimately, whether that thesis converts into operating revenue is the question that Q1 OKLO Earnings Reports framed but cannot answer.

Wall Street’s Verdict on OKLO Earnings Reports

Generally, analyst sentiment on OKLO is constructive but with a wide dispersion that captures the binary nature of the bet. Specifically, fifteen to twenty analysts cover the name, with a Moderate-to-Strong Buy consensus rating. Additionally, the average price target is roughly $92 to $101, depending on the source, implying 20-40% upside from the pre-print level near $78. However, the range from $60 to $150 is unusually wide for a single name.

Analyst Outlook: Institutional Ratings and Price Targets

| Firm | Rating | Target | Core View |

|---|---|---|---|

| Texas Capital | Buy | $150 | Highest target: AI power thesis |

| Tigress Financial | Hold | $130 | Pipeline is strong, execution risk |

| HSBC | Buy | $96 | NRC progress validates roadmap |

| JP Morgan | Neutral | $83 | Initiated May 11; balanced view |

| Goldman Sachs | Neutral | $65 | Cut from $91 in March |

| UBS | Neutral | $60 | Cut from $95 in March |

| Consensus (~15-20 analysts) | Moderate Buy | ~$92–101 | 10 Buy / 5-6 Hold / 0 Sell |

Specifically, the bull case anchors on the AI data center power thesis (McKinsey projects $7 trillion in data center infrastructure investment), the Switch agreement as embedded option value, NRC regulatory progress on accelerated review timelines, and the $2.54B cash position that funds development to first commercial energy.

Conversely, the bear case is straightforward: a pre-revenue stock at an $11B+ market cap, with first operations not expected until late 2027 and full commercial deployment not until the 2030s, requires extraordinary execution to justify current valuation.

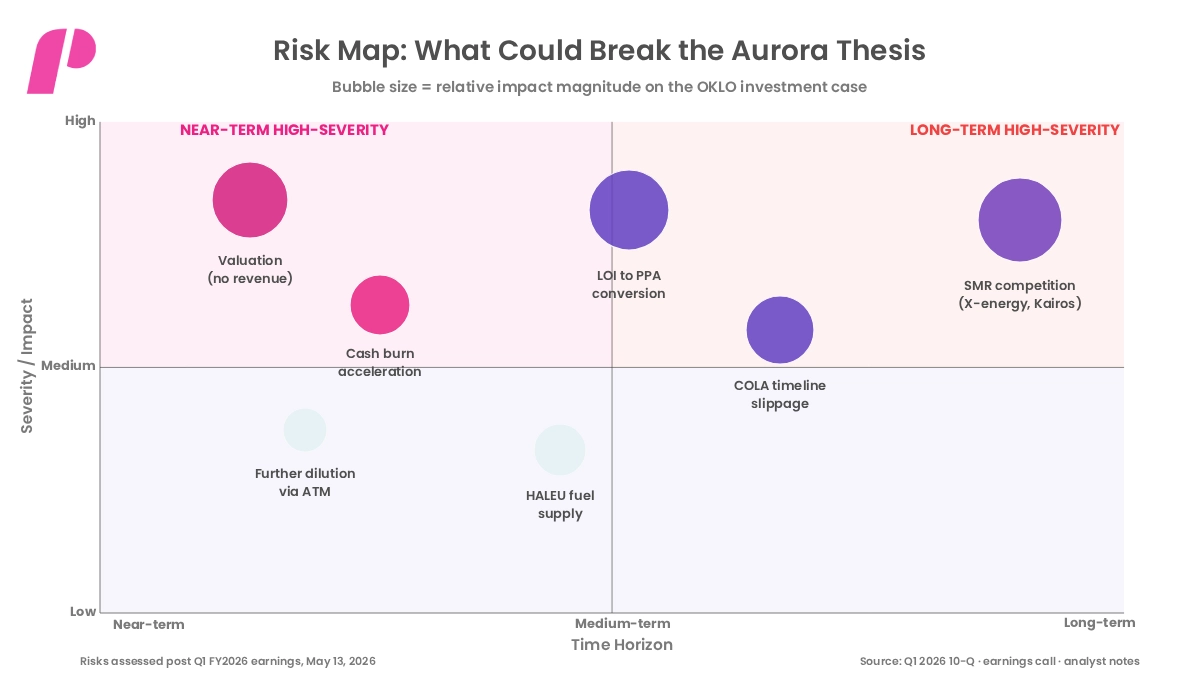

What OKLO Earnings Reports Reveal About the Risks Ahead

Undoubtedly, pre-revenue advanced fission is among the highest-variance investment categories in the public equity markets. Specifically, within that category, OKLO sits at the high-multiple, high-narrative end. Therefore, investors should do any reading of OKLO Earnings Reports against a risk picture that includes regulatory, execution, and competitive dimensions.

Risk Severity vs. Time Horizon for the OKLO Investment Thesis

Assessing Near and Medium Term Cash Flow

Currently, in the near term, the cash burn is the metric to monitor. Specifically, operating cash use was $17.9M and capex was $32.8M in Q1, against a $2.54B cash base. Consequently, that implies a multi-year runway, but the burn rate will accelerate as Aurora-INL construction progresses. However, any quarter where burnout paces expectations could pressure the stock even if regulatory milestones are hit.

Subsequently, in the medium term, the customer conversion question is the operational test. Importantly, none of the 14 GW pipelines is binding. Specifically, the conversion of even one significant LOI—Switch, Meta, or Equinix—into a binding PPA with payment obligations would be a step-change validation event. Conversely, the opposite, a customer publicly walking away, would be a thesis-breaker.

Factoring the Long-Term Existential Risks

Finally, long-term, the existential risks are competitive and regulatory. Specifically, NuScale Power, X-energy (backed by Amazon for 5+ GW), Kairos Power (backed by Google), and TerraPower (backed by Meta and Bill Gates) all develop competing small modular reactor (SMR) or advanced fission technology with their own funding bases. Furthermore, the NRC commercial licensing pathway has never produced an operational advanced fission reactor at scale. As a result, the NRC denied Aurora’s earlier license application in 2022 before the company pivoted to the DOE pilot track for INL. Additionally, HALEU fuel supply (high-assay low-enriched uranium) remains constrained by limited domestic production capacity.

What Actually Happened: The May 12 OKLO Earnings Reports Print

Subsequently, Oklo released Q1 FY2026 results after market close on May 12, 2026. Generally, the headline numbers were in line with expectations, but the cash composition told the real story.

The Reported Scorecard Details

- Revenue: $0 — as expected. Oklo remains pre-commercial with no operating reactors.

- EPS: −$0.19 — matched the −$0.19 Refinitiv consensus exactly; per Benzinga Pro, a $0.01 beat against the −$0.20 figure.

- Net loss: $33.1M — vs. $9.8M in Q1 2025, a 238% widening that reflects accelerating expense ramp ahead of commercial operations.

- R&D: $27.0M and G&A: $24.2M — up sharply on headcount growth and significantly increased stock-based compensation.

- Interest and dividend income: $21.3M — up substantially on the much larger cash and securities base. This is the offsetting line that limited the net loss damage.

- Cash, cash equivalents, and marketable debt securities: $2.54B — total assets $2.70B against modest liabilities of $64.9M. Stockholders’ equity: $2.64B.

- Cash flow: $17.9M of operating cash use, $32.8M for capital expenditures in the quarter.

The Financing Event Impact

Specifically, the financing event was the real news. During Q1, Oklo completed its 2025 at-the-market (ATM) equity program by issuing approximately 12.4 million shares for net proceeds of roughly $1.18 billion. Consequently, that single financing event explains the move from ~$1.4B cash at year-end FY2025 to $2.54B at the end of Q1 and the resulting share count dilution. Therefore, for a company that targets its first commercial operations in late 2027 and won’t generate meaningful revenue until that point, raising cash near the recent rally was the right capital decision. Still, it carries a dilution cost that the bear case can fairly compound.

Post-Print Stock Reaction

Consequently, the stock reaction moved down, then became complicated. Shares fell roughly 5.76% in aftermarket trading on May 12, closing at $75.83, down from a $78.13 close ahead of the print. Specifically, the reaction reflects three things: (1) the loss came in slightly wider than the lowest analyst estimates of net loss (some had projected closer to −$29.5M), (2) capital intensity is rising faster than some models assumed, and (3) the absence of any new binding customer conversion announcement disappointed the most bullish takes.

Confirming the OKLO Earnings Reports Preview Thesis

Furthermore, regarding what the print confirmed about the preview thesis, the print reinforced rather than refuted the central preview claim that investors cannot read OKLO Earnings Reports as conventional earnings reports. Additionally, cash position grew (good), customer pipeline held at 14 GW (neutral, no conversion), regulatory progress was already priced in (NRC PDC pre-print), and burn is accelerating (mildly negative). However, no element of the print materially changed the long-term thesis.

Moreover, what the print has not yet resolved is whether the late-2027 Aurora-INL first-operations target remains intact. Specifically, management reiterated the timeline on the call, but the COLA Phase 1 filing schedule and HALEU fuel fabrication progress at the Aurora Fuel Fabrication Facility will be the next two specific deliverables to watch in Q2.

The Bigger Picture

Ultimately, Oklo has now printed its first-quarter FY2026 results, and the post-mortem confirms what the preview anticipated: this is not a quarter to be measured by earnings per share. It’s a quarter that bought the company another 12 to 24 months of execution runway through dilutive equity, validated its regulatory pathway with the NRC PDC approval that preceded the print, and codified its AI-powered narrative through the Nvidia partnership.

Furthermore, beyond this print, the next twelve months will tell the longer story. Specifically, the Aurora-INL COLA Phase 1 filing, targeted for sometime in 2026, is the next material regulatory milestone. Consequently, the conversion of any 14 GW pipeline LOI into a binding power purchase agreement will be the most important commercial milestone. Additionally, the Aurora-INL groundbreaking has occurred; the next steps are fuel fabrication at the Aurora Fuel Fabrication Facility, reactor vessel manufacturing, and DOE construction authorization.

Evaluating the Total Addressable Market

Ultimately, whether OKLO is a sustainable investment at $76, let alone the $92–101 consensus target, depends on whether commercial advanced fission has reached the point where the regulatory pathway is repeatable, and the customer pipeline is convertible. Furthermore, Bank of America has projected the global nuclear energy sector could expand into a $10 trillion market by 2050, with small modular reactors at the center of that growth. Consequently, if that projection is even directionally right, Oklo’s dual-track regulatory strategy and 14 GW pipeline give it a credible path.

Conversely, if commercial advanced fission lags by even a few years relative to expectations, the market will revalue the stock against a much smaller, more distant total addressable market. Ultimately, the lone takeaway from this round of OKLO Earnings Reports: Oklo has now funded itself through commercial operations on a base-case timeline, secured foundational NRC regulatory approval for its reactor design, and built the most diverse set of customer interest in advanced fission. However, what it has not yet done is convert any of that into recognized revenue, a binding commercial PPA, or an operating reactor. Finally, the May 12 print was one checkpoint in that conversion, while Aurora-INL energization in late 2027 is the next.

If you liked this post make sure to share it!