D-Wave Quantum reports its first-quarter fiscal 2026 results on May 12 before market open. The print arrives at the start of an unusual six-week catalyst stretch that includes the company’s first-ever Investor Day at the New York Stock Exchange on June 1 and Qubits Europe 2026 in London on June 18. Together, that sequence will tell investors whether D-Wave is transitioning from a quantum-computing curiosity into a commercial quantum-computing business. The latest QBTS Earning Reports cycle is the first checkpoint in that sequence.

The setup is unusual. FY2025 was the most successful year in D-Wave’s history: revenue of $24.6 million was up 179% year over year, gross profit margin reached an industry-leading 82.6%, and the cash balance climbed to a record $884.5 million, a 397% increase versus the end of FY2024. Then the calendar turned, and the operating picture got even more interesting. In January 2026 alone, the company closed more bookings than in the entirety of FY2025.

Yet the Q1 FY2026 setup heading into the report looks restrained. Wall Street consensus calls for revenue of just $4.14–5.01 million and an EPS loss of around eight cents. Quantum system sales are recognized on delivery, not order, so the timing gap between bookings and revenue is structural rather than a sign of weakness. The Q1 print will measure how much of the booking surge has begun translating into recognized revenue, deferred revenue, or updated forward guidance.

Shares closed at $21.99 ahead of the print, down about 14% year-to-date but up roughly 55% over the prior 30 days, reflecting sector-wide volatility. The options market is pricing an 18.83% post-earnings move, substantial, even by quantum-stock standards. The mean Wall Street price target sits near $36.91, implying 63% upside from current levels.

The Headline Numbers and What Was Expected

Because Q1 FY2026 actuals print today, the cleanest framing pairs the most recent reported quarter, Q4 FY2025, with the consensus setup for Q1. The two together describe the dollars that have already moved through the income statement and the dollars investors were expecting next.

Financial Performance: Q1 FY2026 Forecast vs. FY2025 Actuals

| Metric | Q4 FY2025 Actual | Q1 FY2026 Consensus | Read |

|---|---|---|---|

| Revenue | $2.8M | $4.14–$5.01M | +50% sequential expected |

| EPS (Non-GAAP) | Loss | −$0.08 | vs. −$0.02 yr ago |

| Adj. EBITDA Loss | −$25.0M | — | Up from −$15.3M YoY |

| Gross Margin (GAAP) | ~82.6% | — | Industry-leading |

| FY2025 Revenue | $24.6M | — | +179% YoY |

| FY2025 Bookings | $18.7M | — | −22% YoY (lumpy) |

| FY26 YTD Bookings (Feb 25) | — | >$32.8M | More than all of FY2025 |

| Cash & Investments | $884.5M | — | Record · +397% YoY |

The bookings-revenue mismatch is the most important relationship in the entire QBTS Earning Reports framework. FY2025 saw revenue more than triple, while bookings declined 22%, because a single eight-figure system sale closed in the prior year, with revenue recognized through 2025 deliveries. The pattern reverses in FY2026: bookings are surging, and the question is when those bookings convert into recognized revenue.

Reading the Pre-Print Scorecard

Three numbers describe D-Wave heading into the May 12 print: the FY2025 revenue base, the Q1 consensus, and the cash position that funds the build to commercial scale.

Consensus vs. Actual Q1 FY2026 Scorecard

The Q4 FY2025 print was indicative. Revenue came in at $2.8 million, missing the consensus estimate of $3.75 million by roughly 26%. EPS missed by 50%. Bookings rebounded sequentially to $13.4 million (up 471% from Q3) thanks to a €10 million capacity agreement with an Italian state-of-the-art quantum facility in Lombardy. The pattern repeated: lumpy revenue, robust bookings, accumulating backlog.

Then, Q1 FY2026 began with a step change. By January 31, D-Wave had announced two transformative deals: a $20 million Advantage2 system sale to Florida Atlantic University with deployment expected by year-end, and a $10 million two-year enterprise quantum-computing-as-a-service (QCaaS) agreement with a Fortune 100 company. By February 25, FY26 year-to-date bookings exceeded $32.8 million, more than all of FY2025.

The structural Takeaway: D-Wave’s business model has two distinct revenue streams. System sales are lumpy and recognized on delivery. QCaaS subscriptions are recurring and recognized on a ratable basis. The Fortune 100 deal in particular signals that the second category is starting to take hold, exactly what Wall Street has been waiting to see.

Revenue Composition: System Sales, QCaaS, and Services

D-Wave generates revenue across four streams, each with very different unit economics. System sales are the largest and lumpiest. QCaaS subscriptions are the most strategically important because they signal recurring commercial adoption. Government and research contracts provide visibility, and professional services attach to deployments.

Revenue Strategy: Recognition, Margin Profiles, and FY2026 Catalysts

| Revenue Stream | Recognition | Margin Profile | FY2026 Catalysts |

|---|---|---|---|

| System Sales (Advantage2) | On delivery | Hardware-typical | FAU $20M deal, EU expansion |

| QCaaS Subscriptions | Ratable | High recurring | Fortune 100 $10M deal |

| Government Contracts | Milestone | Visibility-anchor | US, UK $2.7B, Canada $1B |

| Professional Services | On completion | Project-typical | Attached to the system deals |

| FY2025 GAAP Gross Margin | — | ~82.6% | Software-like profile |

What makes the Fortune 100 QCaaS contract structurally important is the recurring revenue economics. A two-year, $10 million subscription implies roughly $5 million annually, or $1.25 million quarterly, already meaningful relative to D-Wave’s current scale. If even a small subset of the company’s 135+ individual customers (more than 70 commercial enterprises, including two dozen Forbes Global 2000 companies) follow that path, the QCaaS line could begin smoothing the lumpiness that has historically dominated reported revenue.

The Gap Between Bookings and Revenue

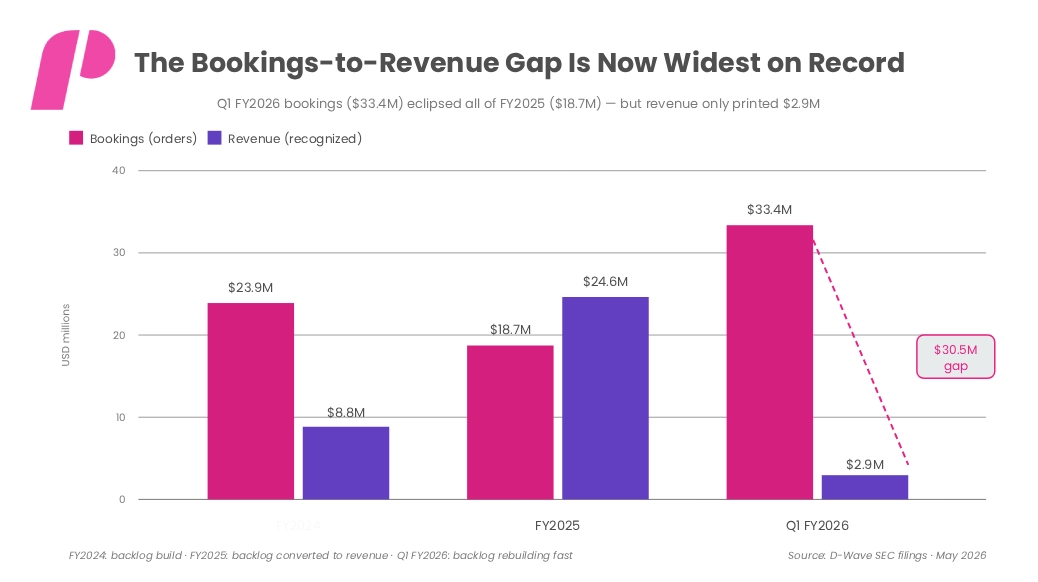

The single most important chart in any review of QBTS Earning Reports is the comparison between bookings (orders received) and revenue (recognized on delivery). When the gap widens, it signals either a delivery bottleneck or an accumulating backlog that will translate into future revenue. When it narrows, it signals operational scaling.

Bookings versus Recognized Revenue, FY2024 through Q1 FY2026

Financial Performance & Backlog Analysis

Three distinct patterns emerge from recent fiscal periods. FY2024 saw bookings ($23.9M) substantially outpace revenue ($8.8M)—a classic backlog build supercharged by a single eight-figure system sale. This momentum shifted in FY2025 as revenue reached $24.6M, finally eclipsing the prior year’s $18.7M in bookings and signaling the successful conversion of that accumulated backlog.

However, the trend has sharpened dramatically in Q1 FY2026. While bookings surged to $33.4M in just three months, revenue “printed” at only $2.9M; consequently, the gap between sales and recognized income is now wider than at any other point in the company’s history on a single-quarter basis.

This represents the “proof window” that the May 12 earnings release was intended to clarify. Investors are specifically looking for:

- Revenue Velocity: How much booking flow is recognized immediately vs. deferred.

- The Near-Term Ramp: The volume rolling into deferred revenue as a signal for H2 performance.

- Guidance: Whether management offers tighter framing for the full-year FY2026 revenue target.

The Customer Roster

D-Wave’s commercial reach is unusually broad for an early-stage quantum company. During FY2025, the company recognized revenue from more than 135 individual customers across more than 70 commercial enterprises, including more than two dozen Forbes Global 2000 companies. The roster spans government, defense, academia, and enterprise, the breadth that competing quantum providers cannot match.

Strategic Ecosystem: Key Customers and Partnership Dynamics

| Customer / Partner | Segment | Deal Size / Type | Strategic Read |

|---|---|---|---|

| Florida Atlantic University | Academia | $20M Advantage2 system | Largest single FY26 booking |

| Fortune 100 Enterprise | Enterprise | $10M 2-yr QCaaS | First major recurring deal |

| Lombardy, Italy | Government | €10M 50% capacity | EU geographic expansion |

| Anduril | Defense | Qubits 2026 speaker | Defense quantum apps |

| AT&T | Telecom | Active customer | Network optimization |

| Davidson Technologies | Defense / Aerospace | Qubits 2026 speaker | Missile defense apps |

| Total Customer Base | All segments | >135 individual | 70+ commercial · 24+ Global 2000 |

The Strategic Pivot: Becoming the Only Dual-Platform Provider

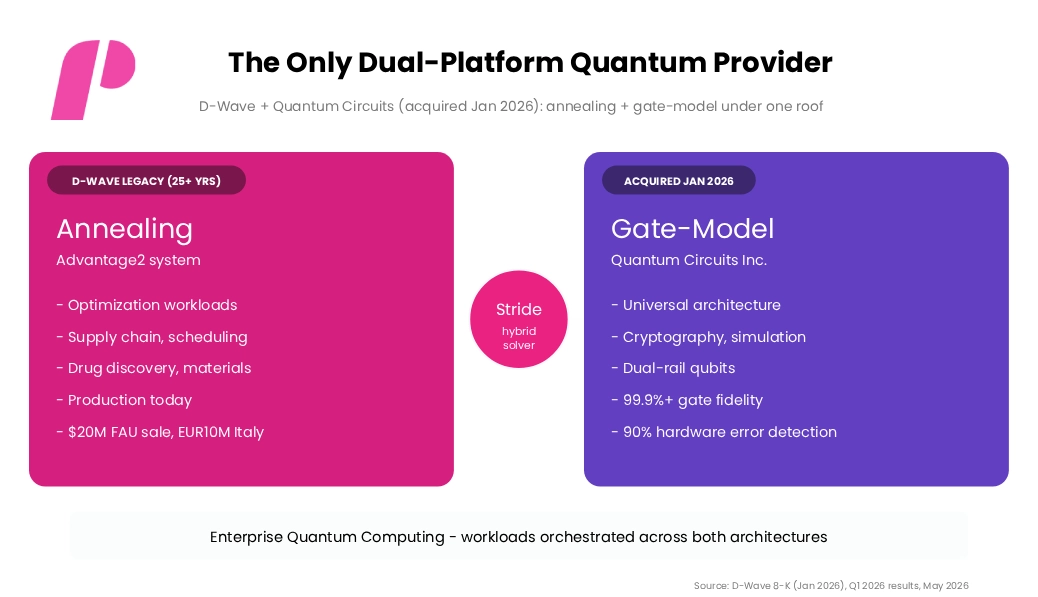

In January 2026, D-Wave completed the acquisition of Quantum Circuits, Inc. (QCi), a developer of error-corrected superconducting gate-model quantum computing systems. The deal is the most consequential strategic move in D-Wave’s history. It makes the company the only quantum computing provider offering both annealing and gate-model platforms, a position that significantly broadens its addressable market and complicates the competitive set facing IonQ, Rigetti, and IBM.

Dual-Platform Strategy: Annealing + Gate-Model + Hybrid Orchestration

The two architectures solve different problems. Annealing, which D-Wave has spent 25+ years engineering through its Advantage2 system, excels at optimization workloads, supply chain routing, drug discovery, materials science, and scheduling. The gate-model quantum architecture that QCi brings is the universal architecture best suited to cryptography, quantum simulation, and the eventual fault-tolerant quantum computing endpoint.

QCi’s specific technical advantage is its dual-rail qubit architecture with built-in erasure detection, which identifies roughly 90% of hardware-level errors. That detection layer enables gate fidelities exceeding 99.9%, the threshold often associated with trapped-ion systems but achieved here at superconducting execution speeds. For D-Wave, owning that technology means it can credibly compete on the gate-model side without having to build it from scratch.

The investment thesis embedded in the platform strategy is clear: enterprise quantum buyers will eventually want both, and D-Wave’s Stride hybrid solver gives it a story for orchestrating workloads across both architectures. Whether that story converts into incremental revenue is the question the Investor Day on June 1 is designed to address.

QBTS Earning Reports: Wall Street’s Verdict

Analyst sentiment on QBTS is unusually constructive for a stock trading at a 12-month forward price-to-sales multiple of approximately 140, well above the quantum-computing peer average of 22x and the broader software sector median of 2.8x. Twelve of fifteen covering analysts rate the stock Buy, with two Holds and no Sells. The consensus price target of $36.91 implies roughly 63% upside from the current $21.99 share price.

Analyst Outlook: Institutional Ratings and Price Targets

| Firm | Rating | Target | Core View |

|---|---|---|---|

| Needham | Buy | $48 | Triple-digit rev growth, expanding demand |

| Rosenblatt | Buy | $43 | Strong Q1 expected; FAU + QCaaS focus |

| Cantor Fitzgerald | Overweight | $40 | Dual-platform strategy positive |

| Roth MKM | Buy | $40 | Commercial adoption trends positive |

| Consensus (15 analysts) | Buy | $36.91 | 13 Buy / 2 Hold / 0 Sell |

| Forward P/S Valuation | — | 140x | vs. 22x peer avg, 2.8x sector |

The bull case rests on triple-digit revenue growth potential, the recurring QCaaS subscription model, sovereign quantum funding ($2.7 billion from the UK and $1 billion from Canada in defense quantum), and a dual-platform competitive position. The bear case is straightforward: at 140x forward sales, the stock is priced for execution that has not yet happened.

What QBTS Earning Reports Reveal About the Risks Ahead

Quantum computing is a high-variance investment category. Even within that category, QBTS sits at the high-multiple end. Any reading of QBTS Earning Reports should be done against a risk picture that includes valuation, execution, and competitive dimensions in roughly that order.

Risk Severity vs. Time Horizon for the QBTS Investment Thesis

In the near term, the 140x forward sales multiple is the binding constraint. A revenue or guidance disappointment on May 12 could easily trigger an 18%+ move down (the options market is pricing this magnitude in either direction). Revenue lumpiness from system-sale timing is structural, not something management can fully smooth, and any quarter in which deliveries slip can read as a fundamental miss, even when bookings tell a different story.

In the medium term, the Quantum Circuits integration is the operational question on which the bull case depends. If the gate-model platform takes longer to commercialize than the optimistic 12–18-month roadmap, the dual-platform story compresses into a narrative rather than an income-statement contribution.

In the long term, the existential risks are competitive. IonQ has triple-digit revenue growth of its own, 755% YoY in Q1, along with international system sales and growing remaining performance obligations. Rigetti and IBM continue to develop superconducting gate-model platforms with their own funding base. And hyperscalers (Microsoft, Google, Amazon) increasingly want to deliver quantum capability through their own clouds rather than buy it from independents. The competitive set is the longest-running tail risk in QBTS Earning Reports.

QBTS Earning Reports: What Actually Happened-The May 12 Print

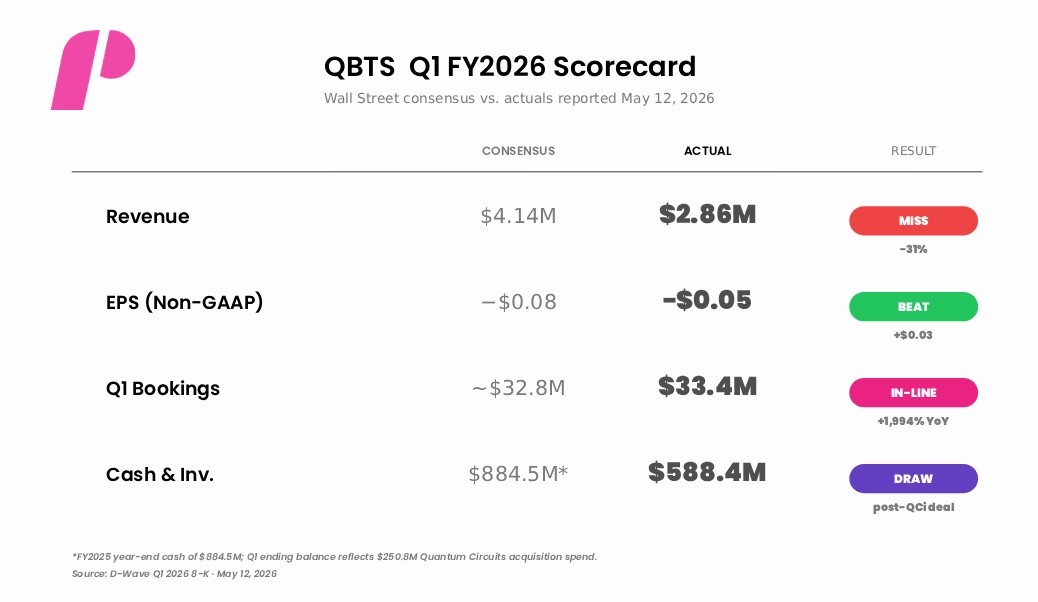

D-Wave reported Q1 FY2026 results before market open on May 12, 2026. The headline numbers split sharply along the lines this preview anticipated: bookings surged, revenue undershot.

The Reported Scorecard

- Revenue: $2.86M — a 30% miss against the $4.14M consensus, and down 81% year over year from a Q1 2025 base of $15.0M that included a $12.6M one-time system sale. Strip out that one-time sale, and the underlying YoY comparison is materially less brutal, but the headline still printed as a miss.

- EPS: −$0.05 — a $0.03 beat against the −$0.08 consensus, a 37.5% positive surprise.

- Net loss: $18.4M vs. $5.4M in Q1 2025; Adjusted EBITDA loss: $32.8M vs. $15.3M.

- Bookings: $33.4M — up 1,994% year over year and 149% sequentially. Includes the $20M FAU system sale and $10M Fortune 100 QCaaS contract previewed above.

- Remaining performance obligations (backlog): $42.4M, up 563% year over year. This metric effectively translates bookings into forward revenue visibility, and it is now larger than all of FY2025 revenue combined.

- Cash & marketable securities: $588.4M, down from $884.5M at year-end FY2025, reflecting the $250.8M deployed for the Quantum Circuits acquisition. Up 93% year over year on a like-for-like basis.

Revenue Composition was the Most Encouraging Detail

For the first time, D-Wave broke out QCaaS subscription revenue cleanly. Q1 revenue was composed of $1.8M in QCaaS subscriptions (the first full quarter of meaningful Fortune 100 contribution) and $1.0M in professional services (up 26% YoY). System sales contributed nothing in the quarter; the FAU deployment is scheduled for later in 2026. The QCaaS line, in particular, is the recurring revenue evidence the bull case has been waiting for.

Commercial revenue accounted for over 73% of the $2.86M total, with revenue recognized from more than 100 individual customers in the quarter alone, over half of them commercial enterprises.

Stock Reaction: Complicated

Shares fell roughly 7.8% in pre-market trading on the revenue miss but reversed direction during the regular session as investors digested the bookings, RPO, and QCaaS details. The stock closed near $22.35, essentially flat versus the pre-print level, well within the 18.83% move the options market had priced in. The market read, in plain language, is that the revenue miss matters less than the backlog signal.

What the Print Confirmed About the Preview Thesis

The central preview claim, that bookings would exceed recognized revenue by a wider margin than ever before, was confirmed by a wide margin. The $30.5M gap between Q1 bookings ($33.4M) and Q1 revenue ($2.86M) is the largest single-quarter divergence in the company’s history.

What remains unresolved is whether the FY2026 revenue trajectory will accelerate as the backlog flows into recognized revenue. Management did not raise or tighten full-year guidance, leaving the Investor Day on June 1 as the next material catalyst for forward framing.

QBTS Earning Reports: The Bigger Picture

D-Wave Quantum has now reported its first-quarter FY2026 results, and the post-mortem confirms most of what the preview anticipated: bookings are surging, revenue recognition lags, and the dual-platform strategy is more visible on the balance sheet (acquisition spend) than on the income statement (system delivery still ahead).

Beyond this print, the next 40 days will tell the longer story. The June 1 Investor Day at the New York Stock Exchange is the venue where management is most likely to articulate a coherent revenue framework that bridges the dual-platform strategy, the QCaaS recurring model, and the government quantum funding tailwind. Qubits Europe 2026, on June 18, is where customer use cases are presented to European sovereign buyers.

Whether QBTS is a sustainable investment at $22, let alone the $37 consensus target, depends on whether quantum computing has actually reached a commercial inflection, not just a funding inflection. McKinsey projects the total economic impact of quantum computing will reach $1.3–2.7 trillion by 2035, and more than 300 global companies are reportedly adopting the technology. If those projections are even directionally right, D-Wave’s dual-platform position is a credible way to participate in that addressable market. If they are not, the stock will be revalued against a much smaller market.

The lone takeaway from this round of QBTS Earning Reports: D-Wave has done the difficult engineering, financing, and customer-acquisition work that was supposed to be the hard part. The Q1 print converted some of that work, $1.8M of recurring QCaaS revenue, into a recognizable software-like line. What it has not yet done is convert the $42.4M backlog into a quarterly income statement that looks like a software company. The May 12 print was one checkpoint in that conversion. Investor Day on June 1 is the next.

If you liked this post make sure to share it!