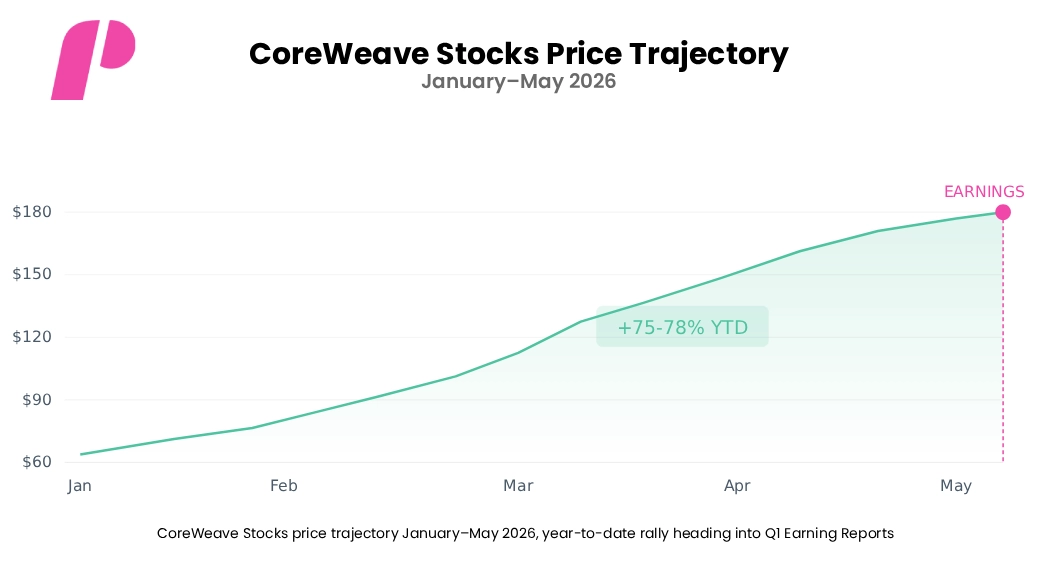

The CoreWeave Earning Reports Story: Three Narratives, One Night

CoreWeave Earning Reports for Q1 2026 represent more than a quarterly financial update. They define which investment narrative leads: backlog conversion, debt refinancing, or customer concentration risk. Investors who track CoreWeave Stocks for a Trading Program must understand all three layers. Each narrative carries a distinct risk-reward profile.

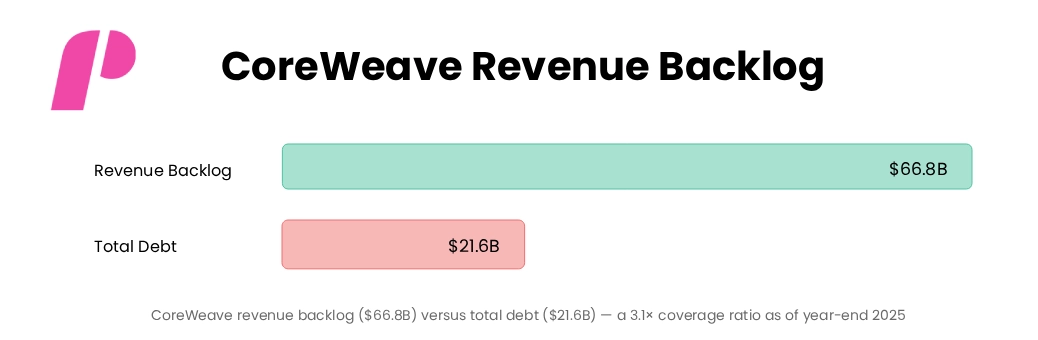

For those building a traded evaluation process around AI infrastructure stocks, Core Weave is a pivotal case study. It is not a profitability story yet. It is a scale story. The company’s $66.8 billion backlog, $21.6 billion in total debt, and its NVIDIA partnership create a uniquely complex picture for CoreWeave’s stock price. Best stocks for beginners typically do not look like this, but understanding this structure builds literacy for the entire AI infrastructure sector.

Insider Selling Tells a Story

Magnetar Funds holds a 10% ownership stake in Core Weave. This fund sold heavily across late April and early May 2026. Form 4 filings reveal roughly $333 million in equity sales during that window. Magnetar also wrote call options at $150, $175, and $180 strikes, expiring December 2026.

Insiders trimming into strength does not signal a company’s collapse. It signals that sophisticated holders view current CoreWeave Stock Prices as a favorable exit point. Any traded evaluation process must flag this selling pattern as a signal worth respecting, not ignoring. It reflects calculated risk management, not panic.

Insider Activity: Magnetar Funds Transactions Surrounding CoreWeave Q1 2026 Earnings

| Date Range | Seller | Activity | Value / Strike | Signal |

|---|---|---|---|---|

| Late Apr 2026 | Magnetar Funds (10% owner) | Equity sales | ~$333M sold | Significant trimming |

| Apr–May 2026 | Magnetar Funds | Call options written | $150 strike | Capped upside bet |

| Apr–May 2026 | Magnetar Funds | Call options written | $175 strike | Capped upside bet |

| Apr–May 2026 | Magnetar Funds | Call options written | $180 strike | Capped upside bet |

| Dec 2026 | Magnetar Funds | Options expiry date | — | All three strikes expire |

Magnetar Funds insider selling and options activity surrounding CoreWeave Q1 2026 Earning Reports

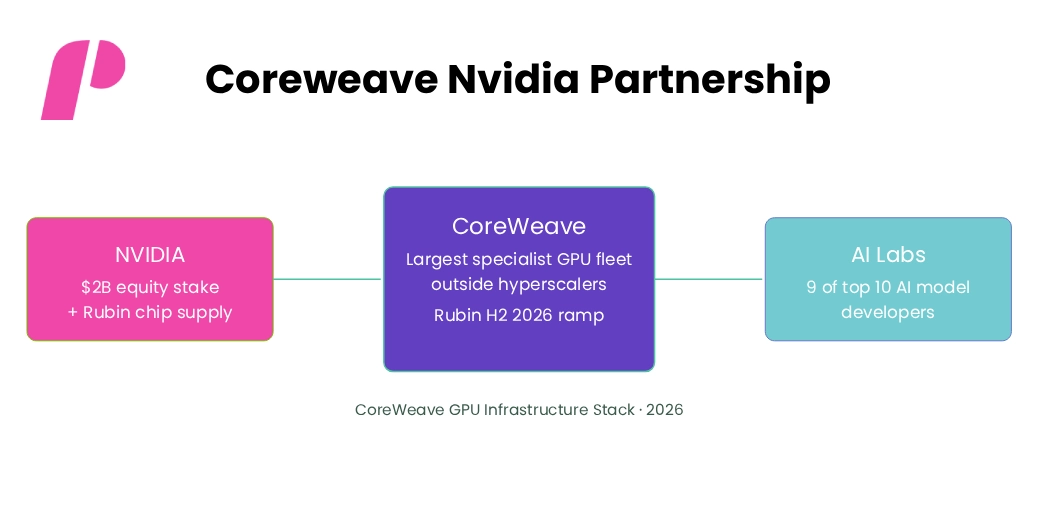

The High-Tech Engine Behind CoreWeave Stocks

CoreWeave runs one of the largest specialized GPU fleets outside the major hyperscalers. NVIDIA holds a meaningful equity stake in the company. NVIDIA invested an additional $2 billion in January 2026, effectively doubling its prior position. Nine of the top ten AI model developers reportedly use CoreWeave infrastructure today.

The company plans to deploy NVIDIA Rubin chips in the second half of 2026. This positions Core Weave ahead of most competitors in the next GPU generation cycle. For investors applying a traded evaluation process to AI infrastructure stocks, this technology roadmap represents the strongest near-term catalyst in the CoreWeave Earning Reports narrative. The Rubin ramp in Q3 is the bull case anchor.

Backlog and Big Deals: The CoreWeave Earning Reports Catalyst

CoreWeave ended 2025 with a $66.8 billion revenue backlog. Jefferies expects April contract wins to lift remaining performance obligations above $95 billion once Q1 reports. This backlog is the foundation of CoreWeave Stocks’ valuation premium versus other AI infrastructure peers. Capacity for 2026 is essentially fully committed at this stage.

Strategic Operations: CoreWeave Major Contract Wins and Revenue Backlog (Q1 2026)

| Client | Deal Type | Value | Equity Component | Significance |

|---|---|---|---|---|

| Meta | Infrastructure expansion | $21B | None disclosed | Largest single deal |

| Jane Street | Compute contract | $6B | $1B equity @ $109/sh | Financial sector anchor |

| Anthropic | Claude AI infrastructure | Undisclosed | None disclosed | AI model validation |

| Total 2025 Backlog | Remaining performance obligations | $66.8B | — | Year-end 2025 baseline |

| Post-April RPO (est.) | Jefferies estimate | >$95B | — | Q1 2026 target milestone |

CoreWeave’s major contract wins and revenue backlog heading into Q1 2026 Earning Reports

The April deals confirm extraordinary enterprise demand. A $21 billion expansion with Meta anchors the quarter. Jane Street signed a $6 billion contract, including a $1 billion equity investment at $109 per share. Anthropic also signed a fresh agreement for Claude infrastructure, a deal that directly validates CoreWeave’s GPU quality at the highest AI model level.

- 2026 capacity is essentially fully committed across all known clients.

- Meta’s $21 billion expansion is the single largest deal in CoreWeave’s history.

- Jane Street’s $109/share equity investment sets a disclosed floor for CoreWeave Stocks’ valuation.

- Anthropic’s Claude infrastructure deal validates CoreWeave’s GPU quality at the frontier AI model tier.

- Jefferies estimates that RPO exceeds $95 billion after the April deals close, the bull-case threshold.

Capital Stack: Cheaper Debt, Bigger Balance Sheet

Investor demand for AI infrastructure debt remains intense in 2026. CoreWeave’s new $3.1 billion leveraged loan attracted roughly $15–$19 billion in orders. Morgan Stanley and MUFG arranged the deal, with margins tightening 50 basis points to 4.5 points above SOFR. The OpenAI and Cohere contracts served as collateral backing for this loan.

Capital Structure: Debt Instruments and Leverage Profile

| Instrument | Size | Rate / Spread | Backing / Notes | Status |

|---|---|---|---|---|

| Leveraged loan | $3.1B | SOFR + 4.5% | OpenAI, Cohere contracts | Oversubscribed |

| Senior unsecured notes | $2.75B | 9.75% | Due 2031 | Priced Apr 2026 |

| Total debt (YE 2025) | $21.6B | Blended | All instruments combined | High leverage |

| 2025 interest expense | $1.229B | +240% YoY | — | Rapidly rising |

| Q1 2026 interest (guided) | $510–$590M | Quarterly | Management guidance | Elevated |

In April, CoreWeave priced an additional $1 billion of 9.75% senior unsecured notes due 2031. This lifted that tranche to $2.75 billion total. Total indebtedness reached $21.6 billion at year-end 2025, a figure central to any CoreWeave Earning Reports analysis. Interest expense alone reached $1.229 billion in 2025, up 240% year over year.

The Profitability Problem in CoreWeave Earning Reports

CoreWeave reported a 2025 net loss of approximately $1.2 billion. Management guides Q1 2026 interest expense at $510–$590 million for that quarter alone. Management expects margins to climb from low single digits in Q1 to low double digits by Q4 2026. That progression requires both disciplined capex and on-schedule backlog conversion.

The 2026 capex guidance stands at $30–$35 billion. This figure exceeds the company’s entire current debt stack. For any investor building a traded evaluation process around CoreWeave Stocks, the profitability math only works if backlog converts to revenue on schedule. One delay creates cascading pressure on interest coverage ratios.

Financial Trajectory: Profitability, Capex, and Q1 2026 Guidance

| Period | Metric | Value | YoY Change | Management Target |

|---|---|---|---|---|

| FY 2025 | Net loss | ~$1.2B | Worse YoY | — |

| FY 2025 | Interest expense | $1.229B | +240% YoY | — |

| Q1 2026 (guided) | Interest expense | $510–$590M | Quarterly | — |

| Q1 2026 (consensus) | EPS loss | –$0.91/share | — | Wall Street est. |

| Q1–Q4 2026 (guided) | EBITDA margin trajectory | Low single → Low double | + | Margin expansion target |

| FY 2026 (guided) | Capex | $30–$35B | Significant increase | Growth investment |

CoreWeave’s profitability trajectory and capex guidance are central to Q1 2026 Earning Reports

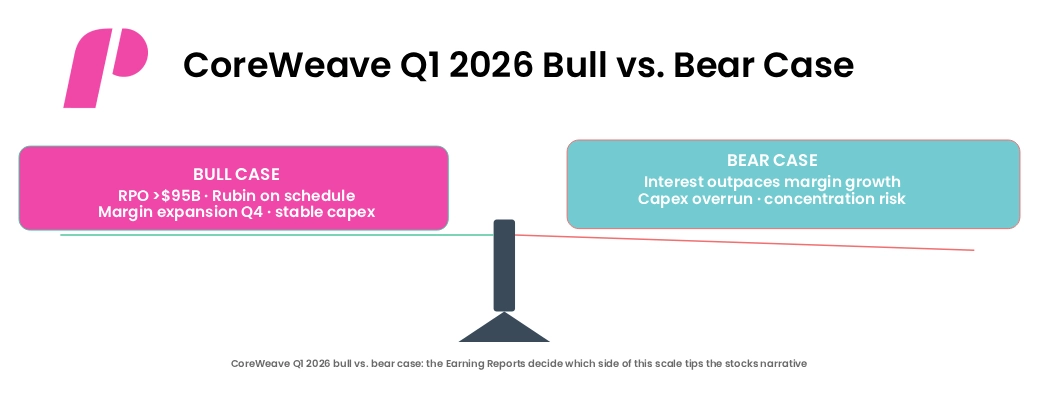

The bull case for CoreWeave Stocks: a $95B+ RPO confirmation and Vera Rubin ramp beginning Q3 2026. The bear case: interest expense outpacing margin expansion through year-end. The CoreWeave Earning Reports on May 7 decide which narrative leads.

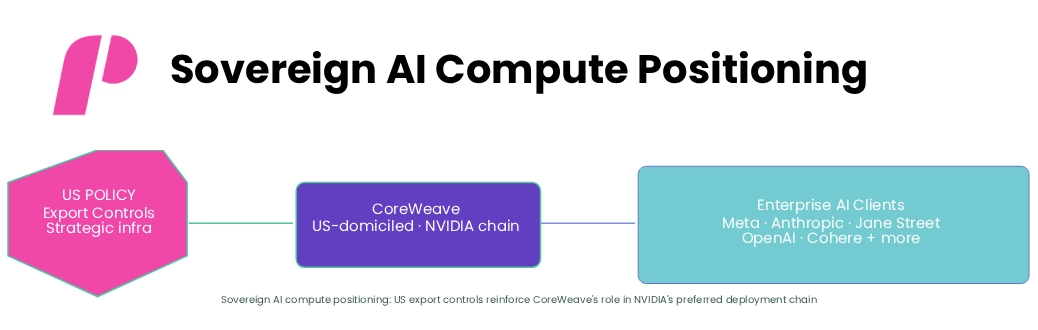

Geopolitics, Cybersecurity, and Sovereign Compute

On the cybersecurity side, CoreWeave runs enterprise-grade workload isolation across its GPU clusters. This capability matters because clients train proprietary AI models on shared physical infrastructure. However, workload isolation is table stakes for any serious AI cloud provider today. Investors applying a traded evaluation process to CoreWeave Stocks should treat it as a necessary baseline, not a differentiated moat.

On the cybersecurity side, CoreWeave runs enterprise-grade workload isolation across its GPU clusters. This capability matters because clients train proprietary AI models on shared physical infrastructure. However, workload isolation is table stakes for any serious AI cloud provider today. Investors applying a traded evaluation process to CoreWeave Stocks should treat it as a necessary baseline, not a differentiated moat.Business Model: From Crypto Mining to AI Stocks Leader

CoreWeave’s leadership team pivoted from crypto mining in 2017 to GPU cloud services for AI workloads. That early agility now produces multi-year contracts with hyperscalers and leading AI research labs. The same flexibility that built CoreWeave also carries forward a structural risk. GPU generations rotate every three to four years, demanding constant capital reinvestment.

The current contract base must fully repay current debt before the next-generation capex wave arrives. For those studying the best stocks for beginners in the AI infrastructure sector, CoreWeave illustrates this capital intensity clearly. A Trading Program built around CoreWeave Stocks must account for this generational GPU replacement cycle as a recurring financial event, not a one-time cost. The business model rewards scale and punishes any slowdown in contract execution.

- CoreWeave pivoted from crypto mining to GPU cloud in 2017, an early, decisive repositioning.

- GPU generations rotate every 3–4 years, creating recurring large-scale reinvestment needs.

- 2026 capex guidance of $30–$35B reflects the current generation’s peak investment cycle.

- Multi-year contracts with Meta, Jane Street, and Anthropic provide revenue visibility across the cycle.

- NVIDIA’s equity stake aligns chip supply priorities with CoreWeave’s infrastructure roadmap.

The Real Question: What CoreWeave Earning Reports Must Answer

CoreWeave’s Earnings Reports for Q1 2026 raise four decisive questions for stock investors. First: Does RPO exceed $95 billion after April deal confirmations? Second: Does Q1 capex guidance remain within the $30–$35 billion annual range? Third: Does margin expansion begin, even modestly, relative to Q4 2025 levels?

Market Scenarios: Bull vs. Bear Case Matrix for CoreWeave (Q1 2026)

| Factor | Bull Case | Bear Case | Current Signal |

|---|---|---|---|

| RPO post-April | >$95B confirmed | <$85B shortfall | Jefferies: $95B+ expected |

| Vera Rubin ramp | Q3 2026 on schedule | Delayed to 2027 | NVIDIA H2 guidance holds |

| Margin trajectory | Q4 low double digits | Stays low single digits | Management guided |

| Interest expense | Stabilizes at Q1 level | Continues rising 20%+ | $510–$590M Q1 guided |

| CoreWeave Stocks move | +18% or more | –18% or more | Options market pricing |

Fourth: Does management address Magnetar’s insider selling directly and credibly? The Magnetar selling matters far less than the capex guidance that lands tonight. CoreWeave Stocks trade on backlog credibility, not current profitability, and tonight’s CoreWeave Earning Reports either confirm or undermine that credibility. Every investor with a Trading Program position in Core Weave must treat this as a binary information event.

If you liked this post make sure to share it!