Wall Street arrived at the May 6 print expecting a strong quarter. What the latest ARM earnings reports delivered was something more important — confirmation that ARM Holdings’ transition from a mobile-architecture company into a foundational AI infrastructure supplier is accelerating, and that demand for its first in-house silicon is already running ahead of the company’s ability to manufacture it.

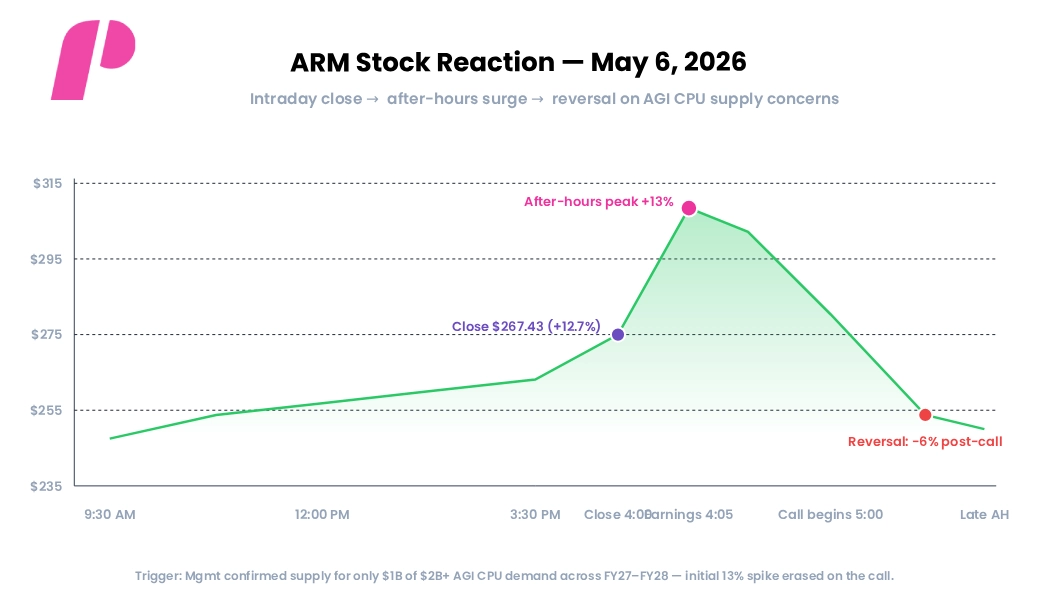

ARM Holdings (NASDAQ: ARM) closed the regular session on May 6, 2026, at $267.43, up roughly 12.7% on the day, before the print pushed shares as much as 13% higher in after-hours trading. That initial enthusiasm reversed sharply once management took the call. By late evening, the stock had given back its gains and was trading roughly 6% below the regular-session close — not because the numbers disappointed, but because management acknowledged supply for the new AGI CPU was outpacing what the company could currently deliver.

Coming into the quarter, ARM stock had rallied roughly 84% year-to-date in 2026. Options markets had implied a 10% post-earnings move. Bull case price targets at UBS, Mizuho, and Wells Fargo had all migrated into the $220–$245 range, while the broader analyst consensus sat closer to $164–$184. The setup, in other words, was already pricing aggressive AI infrastructure assumptions.

The real question is no longer whether ARM is benefiting from AI infrastructure spending. It is whether the AGI CPU ramp, the Compute Subsystems (CSS) flywheel, and the company’s evolving margin structure can grow into a forward multiple north of 100x earnings.

ARM Earnings Reports: The Headline Numbers

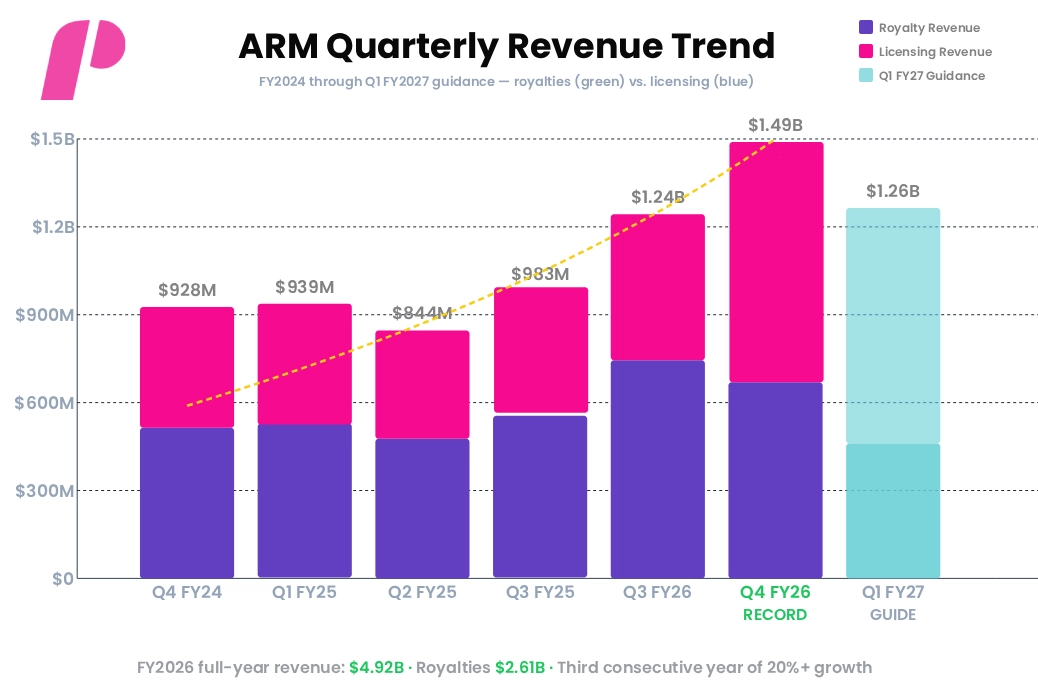

Q4 FY2026 (ended March 31, 2026) was, on every reported metric, the strongest quarter in ARM’s history. Revenue of $1.49 billion grew 20% year over year, marking the third consecutive fiscal year of 20%+ revenue growth since the company’s 2023 IPO. Adjusted (non-GAAP) earnings per share of $0.60 came in two cents above the $0.58 consensus.

Beneath the headline, the mix tells the more interesting story. Licensing revenue rose 29% year over year to $819 million, decisively beating expectations. Royalty revenue climbed 11% to a record $671 million, with data center royalties more than doubling year over year — a key tell for investors trying to size the AI tailwind separately from the cyclical mobile market. For the full fiscal year, ARM reported $4.92 billion in revenue and a record $2.61 billion in royalties.

Earnings Report: Actuals vs. Market Estimates

| Metric | Estimate | Actual | Result / YoY |

|---|---|---|---|

| Total Revenue | $1.47B | $1.49B | Beat · +20% YoY · record |

| Adjusted EPS (non-GAAP) | $0.58 | $0.60 | Beat · record |

| Royalty Revenue | — | $671M | +11% YoY · record |

| Licensing & Other | — | $819M | +29% YoY |

| FY2026 Full-Year Revenue | — | $4.92B | Record · 20%+ growth 3Y |

| Q1 FY2027 Revenue Guide | $1.25B | $1.26B ± $50M | Slightly ahead |

| Q1 FY2027 EPS Guide | — | $0.40 ± $0.04 | Conservative tone |

The Q1 FY2027 guide of $1.26 billion sits sequentially below the record Q4 print but is consistent with the timing of large enterprise licensing deals that typically pull revenue into a single quarter. Importantly, Q1 EPS guidance of $0.40 reflects continued elevated R&D spend tied to the AGI CPU ramp — a reminder that ARM is investing through this transition rather than harvesting it.

After-Hours: A Beat the Market Couldn’t Hold

If the numbers were so strong, why did ARM stock surrender a 13% after-hours gain by the end of the call? The answer reveals something investors should pay close attention to: the constraint on the AGI CPU is no longer customer interest. It is a supply.

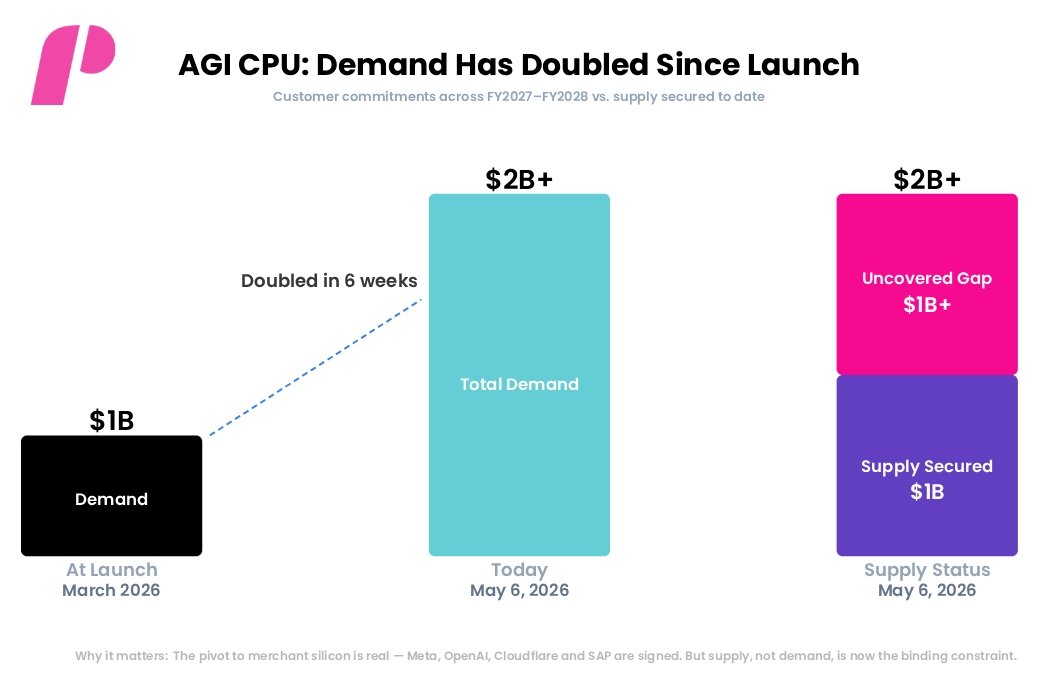

In the shareholder letter that accompanied the print, CEO Rene Haas and CFO Jason Child disclosed that customer demand for the AGI CPU has now exceeded $2 billion in commitments across fiscal 2027 and fiscal 2028 — more than double the demand level disclosed at launch in March. Initial reading: bullish. The market spiked the stock as much as 13% above the close.

On the call, however, management clarified that the company has so far secured manufacturing capacity for only the first $1 billion of that demand. Securing supply for the remaining commitments is in process, but not closed. For a company trading at roughly 109 times forward earnings, even a soft constraint of that size is enough to compress short-term enthusiasm. The ARM earnings reports thus revealed a paradox that bullish investors will recognize: the product is selling faster than the supply chain can deliver.

On the call, however, management clarified that the company has so far secured manufacturing capacity for only the first $1 billion of that demand. Securing supply for the remaining commitments is in process, but not closed. For a company trading at roughly 109 times forward earnings, even a soft constraint of that size is enough to compress short-term enthusiasm. The ARM earnings reports thus revealed a paradox that bullish investors will recognize: the product is selling faster than the supply chain can deliver.

Whether this is interpreted as a bottleneck or as a leading indicator depends on the time horizon. If supply is locked in over the next two quarters, the constraint converts cleanly into FY2027 revenue. If it slips, consensus FY2027 numbers may need to flex — and a stock priced for execution rarely tolerates execution risk well.

Revenue Mix: Why the Business Model Is Changing

ARM does not manufacture chips at scale — historically. It designs the instruction set architectures (ARMv9 today) and licenses them to semiconductor companies, including Apple, Qualcomm, Samsung, MediaTek, and an expanding list of cloud hyperscalers. Every chip shipped using ARM IP generates a recurring royalty. That model has produced a remarkably scalable business: a high-margin, patent-protected toll on a meaningful share of global computing.

What the Q4 numbers show is a deliberate shift in the mix. Licensing revenue is growing materially faster than royalties because customers are increasingly buying full Compute Subsystems (CSS) — pre-integrated, validated platform designs — rather than raw architectural blueprints. CSS deals book substantial upfront revenue and lock in higher per-chip royalty rates downstream.

Financial Performance: Q4 FY2026 Revenue Streams & Margins

| Revenue Stream | Q4 FY2026 | YoY Growth | Strategic Read |

|---|---|---|---|

| Royalty Revenue | $671M | +11% | Recurring · data center >2x YoY |

| Licensing & Other | $819M | +29% | CSS deals + AGI CPU pre-orders |

| Total Revenue | $1.49B | +20% | Record quarter |

| FY2026 Royalty Revenue | $2.61B | Record | Up from $2.17B in FY2025 |

| Adj. Operating Margin (Q4) | ~49% | Down from 53% | R&D investment in AGI CPU/CSS |

The 49% Q4 adjusted operating margin — down from 53% a year earlier — is the trade-off investors should expect through this transition. ARM is funding the AGI CPU ramp, the CSS rollout, and an expanded ecosystem footprint with reinvestment, not buybacks.

The AGI CPU: From IP Licensor to Merchant Silicon

In March 2026, ARM did something it had not done in 35 years: it announced its own chip. The AGI CPU is ARM’s first in-house silicon product, designed specifically for cloud and AI data center workloads, and it represents the most consequential strategic shift in the company’s modern history.

The thesis behind the AGI CPU is straightforward. AI inference and the rise of agentic AI have shifted compute demand back toward CPUs alongside GPUs — and ARM’s architecture leads the industry on performance-per-watt, the metric data center operators care about most as power becomes the binding constraint on AI infrastructure.

Customer reception has been strong enough that demand has doubled in roughly six weeks. At launch, ARM disclosed approximately $1 billion of customer commitments. As of the Q4 print, that figure has grown to more than $2 billion across FY2027 and FY2028. Meta is the lead enterprise partner; OpenAI, Cloudflare, and SAP all signed on as early adopters. Production is expected to ramp through late 2026.

Management reiterated its long-term target of $15 billion in chip revenue and more than $9 in EPS by FY2031, and the company maintains a $25 billion FY2031 total revenue ambition. Those are aggressive numbers — but the AGI CPU pipeline is the first concrete commercial validation that the trajectory is at least directionally credible. The remaining question, raised by the call itself, is whether ARM can secure the foundry and packaging capacity to convert the second $1 billion of demand into shipped silicon.

ARM Earnings Reports: The CSS Customer Roster

The AGI CPU is the headline product, but the broader Compute Subsystems flywheel is the underlying business model change. ARM disclosed it has now signed 19 CSS licenses across 11 enterprise partners. Five customers are already shipping CSS-based chips into commercial markets. CSS agreements carry materially higher royalty rates than traditional architectural licenses — meaning every CSS conversion compounds future royalty economics on top of the upfront license fee.

Strategic Ecosystem: Key Partnerships & Market Penetration

| Partner | Segment | Engagement | Status |

|---|---|---|---|

| Meta | Hyperscale AI | AGI CPU lead customer + CSS | Production targeted late 2026 |

| OpenAI | AI Infrastructure | AGI CPU early adopter | Signed |

| Cloudflare | Edge / CDN | AGI CPU early adopter | Signed |

| SAP | Enterprise Software | AGI CPU early adopter | Signed |

| IBM | Enterprise Compute | Strategic collaboration | Announced March 2026 |

| AWS / Microsoft / Google | Hyperscaler Cloud | Custom ARM-based silicon | Shipping at scale |

| 19 CSS licenses · 11 partners | Multiple | CSS — full platform deals | 5 already shipping |

The Trajectory: Mobile Architecture to AI Infrastructure

Two and a half years ago, ARM was generating quarterly revenue of around $730 million. The company has moved from that base to a $1.49 billion quarter not by riding a single product cycle but by expanding into adjacent compute markets just as those markets entered the steepest portion of their growth curve.

The composition of the curve matters as much as the slope. Royalty revenue has scaled from roughly $400 million per quarter to $671 million, while smartphone unit volumes have actually been a slight headwind — management estimates roughly a 1–2% royalty drag from weak handset shipments. The offset is data center and AI-class workloads, where Q3 FY2026 royalties grew over 100% year on year, and Q4 royalties from data center customers more than doubled again. AI infrastructure spending is now the engine.

The Q1 FY2027 guide of $1.26 billion looks like a step down sequentially, but is best read as the natural lumpiness of large licensing deals being concentrated in particular quarters. Underlying royalty growth — the recurring, harder-to-game part of the business — has continued through the reset.

ARM Earnings Reports: Wall Street’s Divided Verdict

Few large-cap technology stocks entered a print with as wide a spread between bull and bear targets as ARM did on May 6. The latest ARM earnings reports landed against a backdrop where individual analyst targets ranged from $125 (Goldman Sachs Sell) to $255 (high end of UBS-led bull case).

Analyst Outlook: Institutional Price Targets and Core Theses

| Firm / Source | Rating | Target | Core Thesis |

|---|---|---|---|

| UBS | Buy | $245 | Massive AI server CSS ramp + AGI CPU re-rates the model |

| Mizuho | Buy | $230 | AI infrastructure royalty acceleration |

| Wells Fargo | Overweight | $220 | Power-efficient data center positioning |

| Susquehanna | Positive | $210 | Royalty mix shift to ARMv9 |

| HSBC | Buy (upgrade) | $205 | Upgraded from Reduce in March |

| Street Consensus | Buy | ~$182 | AI thesis succeeds, but valuation is contained |

| Goldman Sachs | Sell | $125 | Multiple compression risk at 109x P/E |

The gap between bull and bear is fundamentally about timing and multiples. The bull case assumes the CSS flywheel and AGI CPU ramp scale fast enough to grow into the current multiple. The bear case assumes the transition takes longer, exposing the 109x forward P/E to compression. Both sides looked at the same ARM earnings reports and reached different conclusions — and both will continue to.

Risks Investors Cannot Ignore

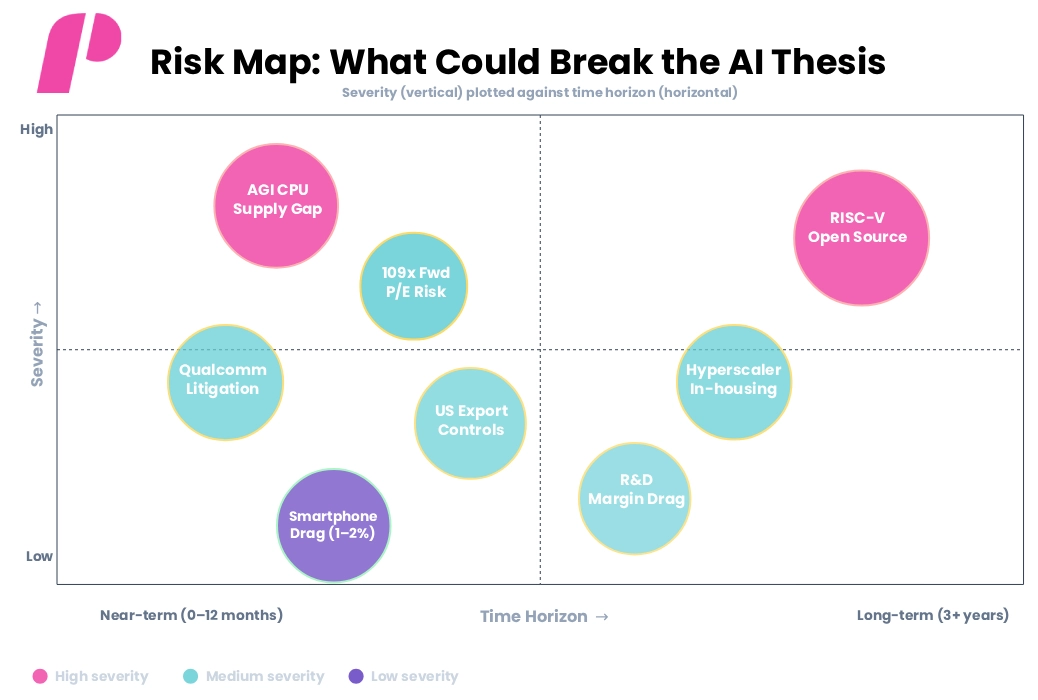

Even the most bullish read of the print does not erase the risks. They are real, they are concentrated at different time horizons, and they explain why Goldman’s $125 price target exists alongside UBS’s $245 price target.

In the near term, the AGI CPU supply gap is the most immediate operational concern. Demand outstripping supply is, on balance, a high-quality problem — but it puts execution pressure on a company whose forward multiple assumes execution. Valuation itself is the second near-term risk: at 109x forward earnings, even a modest miss against expectations could trigger a sharp reset. The Qualcomm/Nuvia litigation, scheduled for trial later in 2026, sits in the medium-severity bucket.

Over the longer horizon, the open-source RISC-V architecture remains the most credible structural threat to ARM’s moat. China is funding RISC-V aggressively to bypass Western IP entirely, and meaningful sovereign-aligned investment in alternative ecosystems is the one outcome that could erode ARM’s licensing economics. US export controls and the semi-independent governance of Arm China continue to introduce operational uncertainty. And while smartphone weakness is creating a 1–2% royalty drag today, that headwind is small enough to be more than offset by AI data center growth — for now.

The Bigger Picture

ARM is no longer simply a smartphone architecture company. Across the latest ARM earnings reports, the throughline is consistent: the royalty engine is moving up-stack into hyperscale computing, enterprise AI deployments, and — for the first time — into ARM’s own merchant silicon. The combination of ARMv9 architecture dominance, an expanding CSS license base, AGI CPU customer commitments above $2 billion, and high-margin recurring royalties forms the most credible long-term AI-infrastructure thesis in the licensing-IP universe.

What May 6 did not resolve is whether the current valuation already reflects all of that opportunity, or only most of it. The print confirmed the thesis is working. The after-hours reversal confirmed the market is pricing perfection. The next several quarters of ARM earnings reports will determine which read is correct: whether AGI CPU supply expands to capture the second billion of demand, whether CSS conversion rates accelerate, and whether data center royalty growth holds at a triple-digit pace.

For investors, the practical takeaway is that ARM remains one of the clearest pure-play exposures to AI infrastructure spending, but it is now one priced for the bull case to keep delivering — quarter after quarter, with very little tolerance for execution slippage. The story is no longer about whether AI is reshaping the semiconductor industry. It is about whether ARM can keep up with the demand that reshaping has created.

Disclaimer: This article is for informational/educational purposes only and is not financial advice or a guarantee of results. Trade The Pool uses simulated funds for evaluation; becoming a funded trader depends on performance and is not guaranteed. Trading involves risk of loss, and past performance does not indicate future results. Services may be restricted in certain jurisdictions. Always conduct independent research and consult a professional before trading.

If you liked this post make sure to share it!