AMD just delivered a Q1 2026 print that crushed expectations. Revenue hit $10.25 billion, up 38% year over year. The company beat consensus by roughly $400 million. Non-GAAP EPS came in at $1.37, above the $1.29 estimate. The stock ripped 20% higher in the next premarket session.

The macro backdrop explains part of the move. Hyperscalers keep raising AI capex budgets every quarter. Enterprise buyers accelerated compute upgrades through the first quarter. AMD captured that spending directly through the Data Center. The AMD stock forecast tightens against consensus after results like this. Investors now ask whether momentum sustains into Q2.

Financial Performance: Quarterly Earnings Growth Analysis (Q1 2025 vs Q1 2026)

| Metric | Q1 2025 | Q1 2026 | YoY Change |

|---|---|---|---|

| Revenue | $7.44B | $10.25B | +38% |

| Gross Profit | $3.99B | $5.69B | +42% |

| Gross Margin | 54% | 55% | +100 bps |

| Operating Income | $1.78B | $2.54B | +43% |

| Net Income | $1.57B | $2.27B | +45% |

| Diluted EPS | $0.96 | $1.37 | +43% |

Why the AMD Forecast Keeps Moving Higher

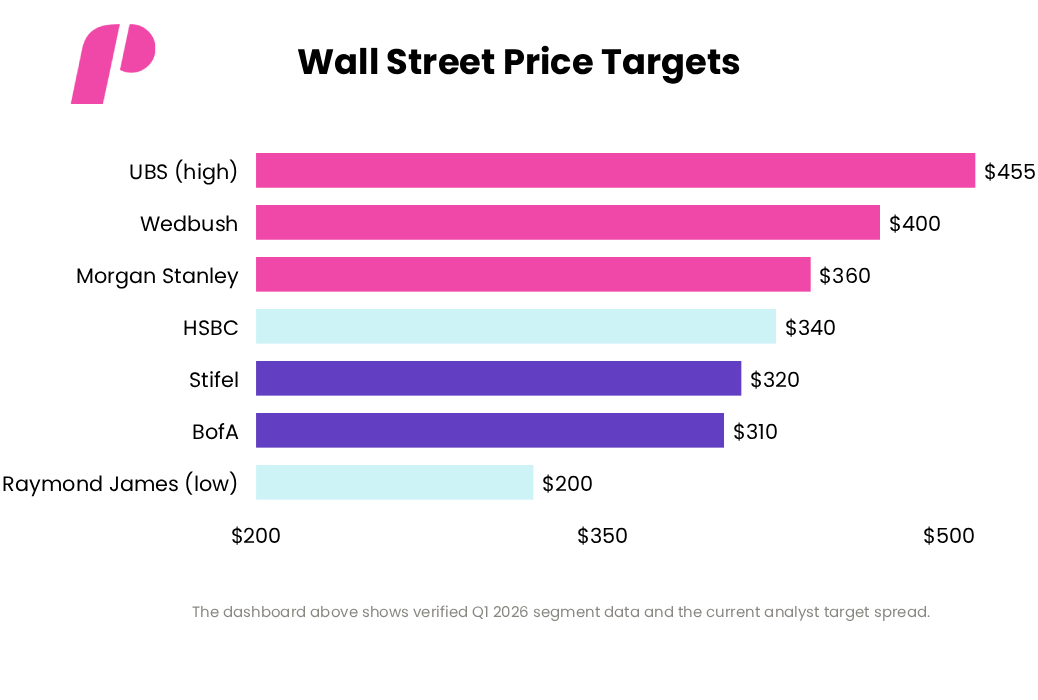

Wall Street targets moved fast in the days around earnings. Morgan Stanley raised its AMD price target to $360 from $255 on May 5. Wedbush set its target at $400, while Raymond James anchors the low end at $200. UBS holds the Street-high target at $455. The consensus sits near $301 across 32 to 34 covering analysts.

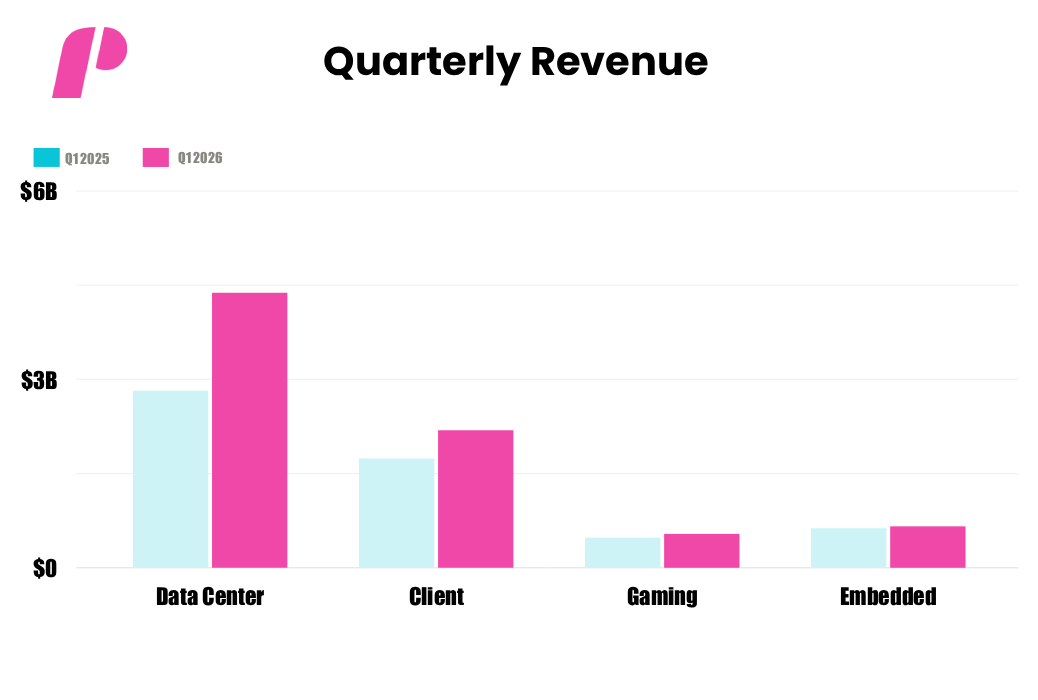

Segment Performance: Revenue and Operating Income by Business Unit

| Segment | Revenue | YoY | Operating Income | Op Margin |

|---|---|---|---|---|

| Data Center | $5,775M | +57% | $1,599M | 28% |

| Client | $2,885M | +26% | (part of C&G) | — |

| Gaming | $720M | +11% | (part of C&G) | — |

| Client & Gaming | $3,605M | +23% | $575M | 16% |

| Embedded | $873M | +6% | $338M | 39% |

| Total | $10,253M | +38% | $2,540M | 24% |

The AMD forecast story has two parts. First, Data Center growth is the engine. Second, supply rather than demand limits the upside. Stifel analyst Ruben Roy named both forces in his April note. Bank of America estimates each gigawatt of AI capacity translates to $15 to $20 billion in AMD revenue. That math drives the upgrades.

AMD Stock Forecast: Geopolitics, Supply Chains, and Industry Trends

Geopolitics still shapes every chipmaker’s quarterly result. AMD took roughly $440 million in net inventory charges in 2025 due to U.S. export controls on the Instinct MI308. The hit shaved about 2 points off non-GAAP operating margin. Management does not expect MI308 China revenue to return.

Lisa Su met Commerce Secretary Howard Lutnick in late April 2026. They discussed AI leadership and export licensing. That meeting matters for the AMD stock forecast over the next two quarters. Hedge fund Trading Programs now model export policy as a discrete risk variable. Domestic manufacturing partnerships through TSMC Arizona reduce some of the exposure. The risk has not disappeared.

Analyst Outlook: Institutional Price Targets and Implied Volatility

| Firm | Target | Direction | Implied Move (from $356.98) |

|---|---|---|---|

| UBS (Acuri) | $455 | Buy | +27% |

| Wedbush | $400 | Buy | +12% |

| DA Davidson | $375 | Buy (Upgrade) | +5% |

| Morgan Stanley | $360 | Overweight | +1% |

| HSBC | $340 | Hold (Downgrade) | −5% |

| Stifel | $320 | Buy | −10% |

| Bank of America | $310 | Buy | −13% |

| Northland | $260 | Market Perform | −27% |

| Raymond James | $200 | Hold | −44% |

| Consensus (32 Analysts) | ~$301 | Buy | −16% |

Innovation and the x86 Ecosystem

AMD and Intel formed the x86 Ecosystem Advisory Group in October 2024. The group released two key standards in 2025 and 2026. APX, the Advanced Performance Extensions, doubles the number of general-purpose registers from 16 to 32. Code compiled with APX contains 10% fewer loads and more than 20% fewer stores than the same code compiled for an Intel 64 baseline.

The second standard is ACE, which is AI Compute Extensions. The original article you sent labeled this “Advanced Computing Extensions” by mistake. ACE standardizes matrix acceleration across x86 CPUs. ACE aims to increase matrix-multiply performance for next-gen x86 chips. Both standards directly target ARM’s data center ambitions. The collaboration matters because ARM threatens both companies in the cloud workload space.

Patent Strategy, Science, and Product Pipeline

AMD continues to spend heavily on R&D. Q1 operating expenses grew 42% year over year to $3.14 billion. The company protects its 3D V-Cache technology behind a deep patent stack. The Ryzen 9 Pro 9965X3D extends that architecture into enterprise CPUs. RDNA4 driver leaks suggest the next discrete GPU generation arrives soon.

The MI450 GPU starts shipping in the second half of 2026. OpenAI and Meta have already signed up for shipments of Helios. Meta announced a multiyear deal involving up to 6 gigawatts of AMD GPUs for AI data centers. The Helios rack-scale system competes with Nvidia’s Vera Rubin platform. Pricing reaches several million dollars per rack at the high end.

Cybersecurity, Linux, and future business models

Hardware-level security now ships standard on EPYC and Ryzen processors. AMD integrates SEV-SNP memory encryption directly into the silicon. The feature attracts buyers in financial services, defense, and regulated healthcare. Enterprise procurement teams compare security feature lists before signing. AMD wins more of those evaluations than it did three years ago.

Linux support continues to improve across consumer and server platforms. Valve pushed AMD to add HDMI 2.1 Linux driver support in 2025. The Zyphra Cloud platform runs on Instinct GPUs across multiple regions. RadixArk launched a $100 million AI infrastructure platform with AMD as a backer. These deals show where investors are finding growth outside the obvious hyperscaler customers.

Strategic Analysis: Growth Catalysts vs. Market Risks

| Catalysts | Risks |

|---|---|

| MI450 ramp begins H2 2026 | Wafer supply tight through 2026 |

| Helios rack-scale system launch | China’s export restrictions on AI GPUs |

| Meta 6 GW multi-year deployment | Nvidia ecosystem moat (CUDA) |

| OpenAI partnership shipping units | Valuation at ~136x trailing P/E |

| Q2 guide implies 46% YoY growth | HSBC cut FY26 AI GPU estimates |

| EPYC server market share gains | Console cycle pressure on semi-custom |

How to execute an analysis trading view on AMD

Beginners often skip the segment breakdown and go straight to headline EPS. That misses the real signal. Look at the Data Center sequential growth first. Then check gross margin direction. Then read the Q2 guide. AMD guided Q2 revenue at $11.2 billion plus or minus $300 million. That figure represents about 46% year-over-year growth and 9% sequential growth.

For beginners, AMD presents a specific lesson on stocks. The headline EPS beat matters less than the quality of the beat. Data Center carried the entire quarter. Client recovered. Gaming and Embedded provided modest tailwinds. AMD stock earnings reports of this shape usually trigger sell-side upgrades within 48 hours. That is exactly what happened on May 5 and 6.

Bottom Line on the AMD Stock Forecast

The AMD stock forecast entering mid-2026 looks structurally bullish but tactically stretched. Data Center growth justifies the multiple expansion of the past 12 months. The MI450 ramp, Helios shipments, and the Meta agreement support a multi-year revenue trajectory. The supply constraint is real and limits short-term upside.

Valuation matters here. AMD trades at roughly 136 times trailing earnings, with a PEG ratio of 0.82. The PEG suggests the price still respects forward growth. Any miss on the Q2 guide would compress the multiple quickly. Long-term holders watch Data Center revenue and gross margin. Short-term traders watch supply commentary on each conference call.

If you liked this post make sure to share it!