Palantir Technologies just delivered the most explosive Palantir earnings reports in company history. Q1 2026 revenue surged 85% year-over-year, the fastest pace since the 2020 direct listing. Furthermore, the data analytics giant now commands a market cap near $350 billion, a valuation reflected in the surge in Palantir’s stock price at recent levels. Wall Street analysts watched every guidance metric crush consensus by remarkable margins.

Investors, analysts, and competitors must now grasp what truly happened in this quarter. This deep-dive analysis unpacks the numbers, strategy, and risks behind the latest Palantir earnings reports. The story spans commercial acceleration, government dominance, and a polarizing leadership stance. Each driver shapes the bull and bear cases moving forward.

Palantir Earnings Reports Crush Q1 2026 Wall Street Expectations

Palantir delivered its fastest revenue growth since its 2020 direct public listing. Total Q1 2026 revenue surged to $1.633 billion. Adjusted earnings per share hit $0.33, easily beating the $0.28 analyst consensus. Revenue cleared the $1.54 billion estimate by nearly 6%. Sequential growth accelerated 16% from Q4 2025. Management called the print the strongest quarter ever recorded.

Net income roughly quadrupled to $870.5 million from $214 million a year earlier. Notably, the Rule of 40 score soared to a stunning 145% in Q1 2026. Adjusted free cash flow reached $925 million in just three months. Palantir ended Q1 with $8.0 billion in cash and zero debt. GAAP operating margin expanded to 46% during the quarter. Such efficiency reflects disciplined capital allocation across every business unit.

Financial Performance: Q1 2026 Earnings & Growth Metrics

| Metric | Q1 2026 Result | Year-over-Year Change |

|---|---|---|

| Total Revenue | $1.633B | +85% |

| US Revenue | $1.282B | +104% |

| US Commercial Revenue | $595M | +133% |

| US Government Revenue | $687M | +84% |

| Net Income | $871M | ~4x increase |

| Adjusted EPS | $0.33 | Beat by 18% |

| Adjusted FCF | $925M | 57% margin |

| Rule of 40 Score | 145% | Industry-leading |

Decoding Palantir Earnings Reports: Revenue Breakdown by Segment

US revenue led the charge by crossing 100% growth for the first time ever. Total US revenue jumped 104% to $1.282 billion in a single quarter. Commercial customers fueled the acceleration most aggressively this period. The segment grew 133% year-over-year to $595 million. Domestic momentum now defines the entire growth narrative. International revenue, by contrast, lagged the US surge meaningfully.

Government revenue remained the largest pillar at $687 million for the period. Specifically, US government sales climbed 84% as defense agencies expanded contracts dramatically. Palantir closed 206 deals worth at least $1 million during the quarter. Additionally, 47 deals exceeded $10 million in contract value. Total contract value reached $2.41 billion, up 61% year-over-year. These bookings translate into multi-year revenue visibility for shareholders.

Palantir Earnings Reports Reveal Explosive Commercial Growth

The commercial flywheel now defines every Palantir earnings report cycle. AIP bootcamps shorten sales cycles dramatically across enterprise customers. Consequently, US commercial customers grew 42% year-over-year to 615 active accounts. Trailing 12-month US commercial TCV bookings reached $4.7 billion. Additionally, the company closed 139 US commercial deals above $1 million in Q1.

Remaining deal value tells an even bigger story for long-term investors today. Indeed, US commercial RDV climbed 112% year-over-year to $4.92 billion at quarter-end. This figure represents future revenue already contractually locked in across customers. Therefore, growth visibility now extends well into 2027 and beyond. Bookings momentum suggests management’s 120% commercial guidance carries genuine credibility. Few software peers can match this commercial trajectory at scale.

Why Palantir Earnings Reports Boost Government Revenue

Government contracts continue anchoring Palantir’s predictable revenue base each quarter. The Gotham platform remains the workhorse for Western intelligence agencies worldwide. It tracks adversaries and manages battlefield logistics in real time. The Pentagon, ICE, Army, and Air Force all rely on Gotham daily. Long procurement cycles create durable, multi-year revenue streams.

Recent contract wins illustrate Palantir’s expanding federal footprint quite clearly. For example, the company landed a $300 million USDA deal to safeguard food supply data. Defense spending tailwinds continue boosting forward bookings significantly. Moreover, allied nations increasingly procure Palantir software for sovereign defense needs. The UK, Israel, Japan, and Germany all expanded purchases recently. International defense represents the next large growth vector.

Patent Portfolio: The Hidden Strength in Palantir Earnings Reports

A robust patent portfolio quietly fortifies every Palantir earnings report cycle. The company holds hundreds of patents across data analytics and artificial intelligence. Specifically, Palantir aggressively patents its ontology-driven data modeling techniques. These filings build a deep economic moat against would-be rivals. Investors often overlook this structural advantage entirely.

Patent analysis reveals an intense focus on machine learning workflows and pipelines. Importantly, this intellectual property prevents rivals from cloning Foundry’s core architecture. Legal teams defend filings with aggressive enforcement actions when needed. As a result, competitors struggle to replicate Palantir’s integrated AI stack. Switching costs grow even higher once customers commit. The moat compounds with every new patent grant filed.

Cybersecurity and Apollo: Foundations of Palantir Earnings Reports

Cybersecurity sits at the core of Palantir’s enterprise sales pitch today. Apollo delivers continuous, secure software deployment across air-gapped environments. Few competitors can match this capability for classified federal networks. Highly regulated industries, therefore, trust Palantir with their most sensitive workflows. The platform handles secrets at FedRAMP High and IL6 levels.

Banks, hospitals, and energy utilities all deploy Foundry for governed AI use. Therefore, cybersecurity strengths translate directly into measurable commercial earnings power. The platform meets the strictest federal security standards available. Consequently, switching costs become enormous after enterprise-wide deployment. Compliance officers cite Palantir as a key risk-reduction lever. This trust unlocks large, multi-year enterprise agreements.

Geopolitics Drive Palantir Earnings Reports Higher

Global friction translates directly into Palantir contract velocity each quarter. President Trump’s proposed $1.5 trillion defense budget significantly lifts Palantir’s revenue outlook. Western intelligence agencies depend on Gotham for mission-critical operations. Allied procurement programs now span every major NATO member nation. Israel and Ukraine both deploy Palantir at the front lines.

Geostrategic alignment shapes every major deal that Palantir signs today. The company explicitly refuses business with adversarial regimes worldwide. This stance reinforces deep trust with the US and allied governments. Subsequently, defense pipelines expand even during commercial slowdowns elsewhere. Karp publicly champions Western technological supremacy at every opportunity. The positioning attracts mission-driven engineers and patriotic capital alike.

Macroeconomic Forces Behind Palantir Earnings Reports

High interest rates push enterprises toward measurable software ROI immediately. Palantir Foundry delivers documented cost savings within months of deployment. This value proposition resonates with cost-conscious CFOs in every sector. Hence, AIP demand accelerated even as broader IT budgets tightened. Boards now demand AI initiatives with concrete payback periods.

However, competition remains a persistent headwind for the company today. Google, Microsoft, Databricks, and Snowflake all target similar enterprise workloads. Each rival pushes aggressive AI feature roadmaps every single quarter. Consequently, Palantir must keep innovating to defend its premium pricing. Hyperscalers leverage existing cloud relationships ruthlessly. Therefore, sales execution must remain razor sharp going forward.

Competitive Landscape: Palantir Differentiators vs. Legacy Platforms

| Competitor | Primary Threat | Palantir Differentiator |

|---|---|---|

| Microsoft Fabric | Enterprise data fabric | Closed-loop ontology |

| Google Cloud | Cheap data warehousing | Operational AI workflows |

| Databricks | Lakehouse + MLOps | Defense-grade security |

| Snowflake | Data sharing platform | Real-world action layer |

| C3.ai | Industrial AI applications | Vertical depth + government |

Leadership and Culture Shaping Palantir Earnings Reports

CEO Alex Karp drives a polarizing yet remarkably effective company culture. His unapologetic defense of Western interests filters talent decisively at every level. A controversial company manifesto recently fueled fierce public debate online. Critics labeled certain corporate stances as confrontational and ideological. Supporters call the same posture refreshingly honest in a vague industry.

Nevertheless, leadership ignored backlash and doubled down on flawless execution. Revenue per employee just hit an extraordinary $1.5 million on an annual basis. That figure outpaces nearly every public software peer in the world. Clearly, the polarizing culture produces measurable financial output every quarter. Karp’s quarterly letters remain mandatory reading on Wall Street. Moreover, employee loyalty appears unusually strong despite outside criticism.

Forward Guidance: What Palantir Earnings Reports Promise Next

Palantir raised full-year 2026 revenue guidance after Q1’s blowout performance. Management now expects $7.65 billion to $7.66 billion in 2026 revenue. That figure represents 71% annual growth at the midpoint. Wall Street consensus previously sat at just $7.27 billion. Therefore, the raise lifted the bar by roughly $360 million in a quarter.

Quarterly guidance also crushed expectations across every individual line item. For Q2 2026, leadership projects $1.8 billion in revenue, well above the $1.68 billion consensus. US commercial growth guidance jumped to 120% for the full year. Adjusted free cash flow guidance climbed to $4.2-$4.4 billion. Such aggressive numbers signal confidence in pipeline conversion.

Forward Guidance: FY 2026 Outlook vs. Market Consensus

| Guidance Metric | New Outlook | Prior / Consensus |

|---|---|---|

| Total FY 2026 Revenue | $7.65B-$7.66B | $7.27B consensus |

| FY 2026 Growth Rate | 71% YoY | ~62% prior |

| US Commercial Growth | 120%+ | ~100% prior |

| Adjusted FCF | $4.2B-$4.4B | $3.8B prior |

| Q2 2026 Revenue | ~$1.80B | $1.68B consensus |

Valuation Debate Following Palantir Earnings Reports

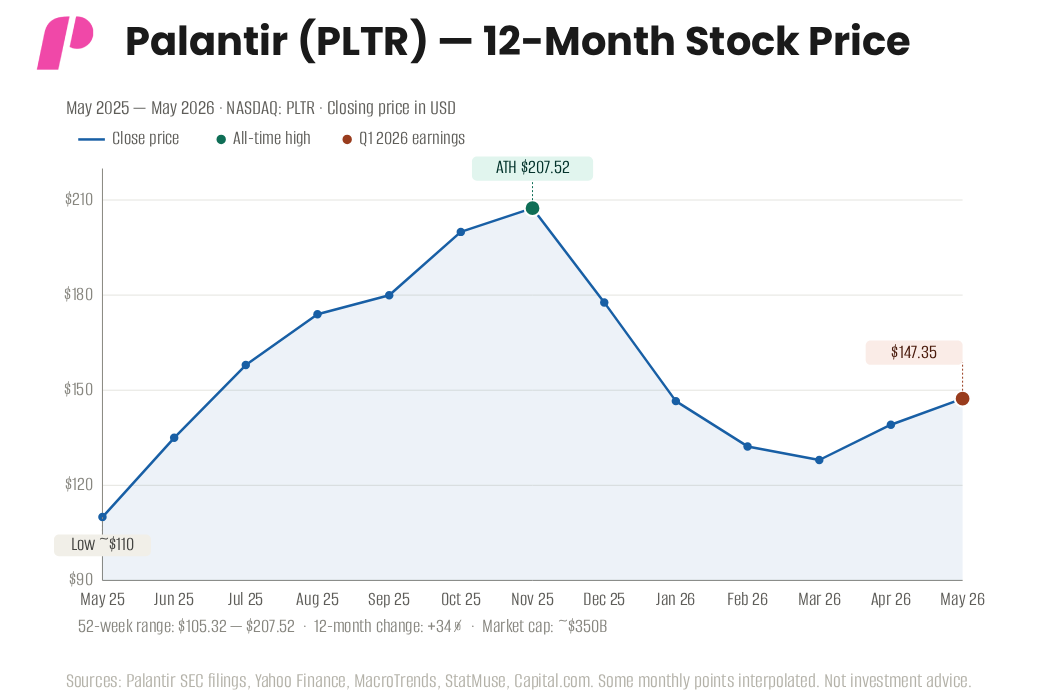

Palantir trades around $144 with a market cap of nearly $350 billion currently. The price-to-earnings ratio sits above 200, signaling extreme growth expectations. Bulls argue the Rule of 40 score justifies the rich premium clearly. Bears warn that valuation already prices in flawless multi-year execution. Morningstar still pegs fair value much lower than current levels.

The stock sits roughly 30% below its 52-week high of $207.52 today. Therefore, investor sentiment remains divided despite the stellar Palantir earnings reports. Aftermarket trading saw only modest gains following the impressive print. Analysts believe shares need 18-24 months to grow into the multiple. Options traders reportedly hedge aggressively against further drawdowns.

Risk Factors Investors Must Watch Closely

Concentration risk remains the most pressing concern for new buyers today. A handful of mega-deals still drive a meaningful share of quarterly upside. US commercial growth must sustain a triple-digit pace through 2026 confidently. Additionally, government budget cycles always introduce procurement timing risk. Continuing resolutions can delay scheduled awards meaningfully.

Competitive pressure will only intensify across the AI platform landscape. Hyperscalers like Microsoft and Google bundle competing analytics into existing cloud contracts. Palantir must keep proving differentiated value at premium prices clearly. Otherwise, commercial churn could threaten the current growth narrative quickly. Investor scrutiny on valuation multiples will likely tighten further.

Final Thoughts

The latest Palantir earnings reports confirm dominant momentum across every key segment. Commercial growth crossed triple digits while government revenue remained durably strong. Ultimately, the $8 billion cash pile and 145% Rule of 40 separate Palantir from every software peer. This combination of growth and profitability remains genuinely rare in technology.

Risks remain meaningful for long-term shareholders nonetheless. Specifically, valuation, competition, and geopolitical exposure all warrant ongoing scrutiny each quarter. Still, Q1 2026 set a new performance benchmark for the company. Future Palantir earnings reports will ultimately determine whether $350 billion proves sustainable. Execution from here must remain near-flawless to justify expectations.

Disclaimer: This article is for informational/educational purposes only and is not financial advice or a guarantee of results. Trade The Pool uses simulated funds for evaluation; becoming a funded trader depends on performance and is not guaranteed. Trading involves risk of loss, and past performance does not indicate future results. Services may be restricted in certain jurisdictions. Always conduct independent research and consult a professional before trading.

If you liked this post make sure to share it!