Now that we all know that the Fed can (and does) lower the interest rate to boost economic growth and employment or it can raise it to fight inflation, let’s talk a little about the other, relatively new – power that the FED has at its disposal: money printing. A.k.a. Quantitative Easing (QE).

The power of printing money whenever you need it would seem like a dream for anyone but, as we all know, with great power comes great responsibility and this is no exception.

Powers and responsibilities regarding QE are the focus of this article – the fourth of the “Federal Reserve System” series – and to better comprehend it all, we need to take a quick jump back in time to 2008.

Heck of a jump, I know but, then again, a heck of a year too; stay with me.

Where did it all start

During the economic crisis of 2008, GDP fell by 4.3% making it the worst recession in 60 years.

In the US alone, 8.8 million people lost their jobs and 6 million houses were repossessed. In Wall Street, the bear market lasted 17 months and was enough to “rob” the S&P 500 of half its value.

On 15 September 2008, Lehman Brothers, the World’s fourth-largest investment bank, shocked the World by filing for bankruptcy. The stock market crashed. People kept losing their jobs. Banks did not trust other banks and businesses and refused to lend to either as well as to the public.

The recession that changed everything

2008 was the year (and a half) of the Great Recession but it was also the year the FED made two important, “everything-changing” decisions.

- The first decision was made upon the realization that, given the intricacies of “investment globalization” and the amount of capital it represents, some businesses are, literally, “too big to fail”.

It could be argued that the ramifications of this decision are anti-capitalism and going against “free market spirit” (and it was argued. Animatedly too) but from the FED’s perspective, protecting the economy and maximizing employment is part of the mandate and it must adhere to it… apparently, at all costs.

The concept referred primarily to banks and large insurance companies but there is no real clear restriction and once Pandora’s box is open, there is no putting anything back.

- The second decision the FED took might have been viewed as even more drastic and it was made after realizing that the economy risked imploding due to a lack of credit and capital. It lowered its interest rate target from 4.5% at the end of 2007 to just 2% in September 2008 but the cost of credit wasn’t the issue; trust and credibility were. Banks were determined to avoid any risk amid the turmoil and kept refusing to lend to one another as well as to businesses. That’s when the FED created a new way to fight a recession and “printed” its way out of it.

Quantitative Easing (QE)

In previous articles of this series, we have talked about how the FED can change the interest rate to influence the availability and cost of credit. We know that to do this, the FED raises or lowers the interest it charges to other banks (the Federal Funds Rate) and that this creates a ripple effect that affects the interest rate on all the other loans.

But there is another way to inject capital into the markets and the economy; a faster and more efficient way: Quantitative Easing.

Starting in Japan and used in the US for the first time during the 2008 crisis, the process consists of the Central Bank buying Government bonds and other securities (mostly mortgage-backed) from the open market and paying for them with money that the FED can digitally create themselves.

This powerful monetary policy has the double effect of making bonds more expensive (and, therefore, stock more attractive) and injecting a huge amount of money into the economy which provides banks with a greater incentive to lend.

Being able to create money from seemingly thin air – added to that of manipulating the interest rates – would undoubtedly seem like the best “superpower” to have to prevent any recession, yet the new policy was, at first, received with anger, criticism and protests with tens of thousands of people marching in the streets.

In 2008, it wasn’t easy – and it will never be easy – for the FED and the Government to explain to “The People” why some businesses could not be allowed to fail. It was hard to explain why huge investment banks had to be saved even if considered “the cause of the crisis”. And, it was hard to explain to “ The People” why they had to be forced through a long period of austerity and forced to help those businesses against their will.

It is all very understandable.

However, the truth is that it is really hard to imagine what the outcome would have been had the FED not intervened.

The American economy is notarially strong and resilient but the pillars that support it can be a little more brittle and need regular management. That’s what the FED does and, as we now know, that’s the FOMC mandate.

During the Great Recession, the FED QE managed to finance Government’s guarantee and bailouts worth £498 billion which helped restore trust and sentiment in the market. The abundance of funds, higher cost of bonds and low-interest rates have all pushed banks to compete with one another for a share of the lending market.

The economy flourished and kept flourishing. GDP increased year after year while the stock market reached a higher and higher level. Unemployment was low and “The People” had higher incomes and started spending more. Way more.

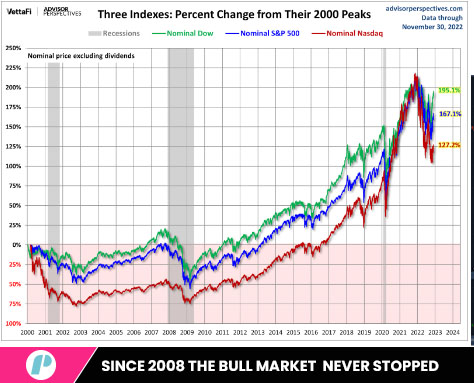

Everything was great. The recession was over and it was the beginning of a bull market that carried on and reached its highest level in 2021.

There has to be a catch

Of course there is.

It is true; since the 2008 crisis, the bull market and “the happy days” have never stopped but it is also true that neither has the “printing” nor is the ultra-low interest rate.

The FED has continued quantitative easing without interruption since 2007, when it first introduced the policy. This, many argue, gives the American economy an artificial advantage which may not always reflect real economic growth and can, therefore, result in high inflation, market bubbles and public discontent.

In the article on “Inflation”, we have already seen the damages that “too much money” in the system can create to the economy if it’s not equally matched by a growth in GDP. In this article, as well as in the one on “unemployment”, we’ve seen the troubles that can occur when the money in the system is instead not enough.

The Fed’s set of tools is powerful but its job is not simple. The perfect equilibrium of economic bliss is hard to find – let alone achieve – in a market that is, by nature, free.

The current economic downturn and high inflation are the newest challenges for the FED.

The money printed in existence and put in circulation during the 2008 recession is shadowed by the money created during the Covid pandemic.

High inflation was to be expected; the war in Europe perhaps wasn’t.

With the Russian invasion of Ukraine, the high inflation level post-pandemic – which was thought to be only temporary – escalated due to sanctions and major disruption in the supply of energy and food commodities. The Fed had to take hard and unpopular decisions and it certainly did so but… this is a topic for another future article. Stay tuned.

![]() Learn more about the fundamental aspect of trading in our fundamentals category

Learn more about the fundamental aspect of trading in our fundamentals category

If you liked this post make sure to share it!