Broadcom stock (AVGO) is not a company you stumble across. You find it when you start asking serious questions about where AI infrastructure money actually flows — and who collects it. The answer, consistently, points back to Broadcom. For traders and investors, AVGO stock offers something rare: a company sitting at the exact intersection of two massive spending cycles simultaneously. AI chip demand is accelerating. Enterprise software subscriptions are compounding. Few companies in the semiconductor space carry both engines at once. Broadcom is not just a chip company — it is a critical infrastructure provider for the world’s largest cloud platforms.

Broadcom Inc. is headquartered in Palo Alto, California. Founded in 1961, the company designs and supplies semiconductor solutions and enterprise software for data centers, networking, storage, and AI applications. It operates two segments: Semiconductor Solutions and Infrastructure Software. The 2023 VMware acquisition fundamentally changed its financial profile. Today, Broadcom serves Google, Microsoft, Meta, and Amazon as a mission-critical infrastructure partner — embedded deeply enough that switching costs are prohibitive.

Broadcom at a Glance

Corporate Profile: Broadcom Inc. (AVGO) Overview

| Metric | Detail |

|---|---|

| Founded | 1961 |

| Headquarters | Palo Alto, California |

| Ticker | AVGO (NASDAQ) |

| Market Cap (June 2026) | ~$1.83 trillion |

| Core Segments | Semiconductor Solutions, Infrastructure Software |

| Key Clients | Google, Microsoft, Meta, Amazon |

| Q2 FY2026 Revenue | $22.2 billion (record, +48% YoY) |

| Quarterly Dividend | $0.65 per share |

What Makes Broadcom Stock Different

Most chip stocks live and die by GPU demand cycles. Broadcom stock plays a different game. The company supplies custom AI chips — called ASICs — built specifically for each hyperscaler’s workload. Google, Microsoft, and Meta do not buy off-the-shelf silicon from Broadcom. They co-develop it. That distinction matters enormously for revenue visibility and competitive moat. AVGO stock is a direct proxy for AI infrastructure spending — not a downstream beneficiary, but an upstream architect of it. When Google builds its next generation of Tensor Processing Units, Broadcom is in the room designing them. That relationship does not get replaced overnight.

Revenue Visibility

This custom silicon model creates something pure GPU suppliers cannot offer: multi-year design cycles that lock in revenue visibility before a single chip ships. Every new generation of hyperscaler AI infrastructure requires a new design engagement with Broadcom. Each engagement extends the revenue runway by two to three years. For traders evaluating AI stocks on a longer time horizon, this structural advantage separates AVGO stock from the rest of the sector.

Q2 FY2026 Earnings: The Numbers Were Strong. The Reaction Was Not.

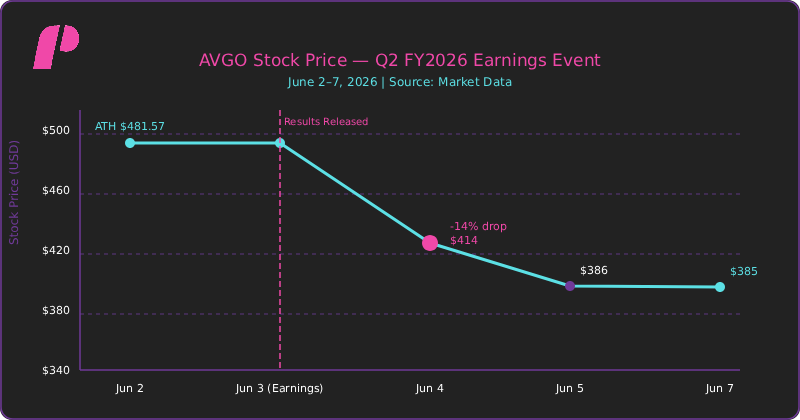

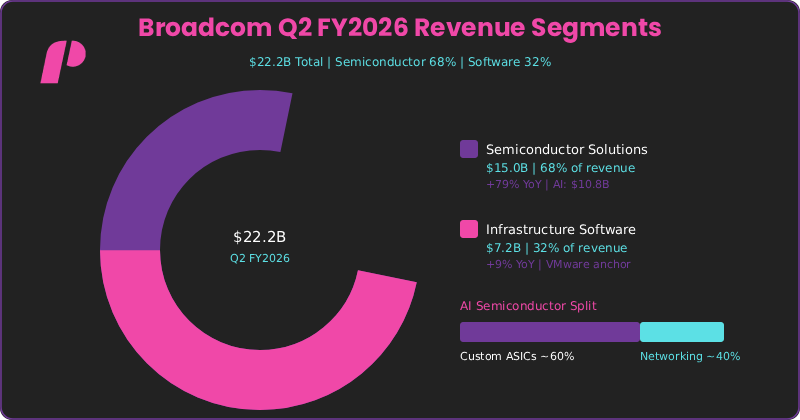

Broadcom delivered record results on June 3, 2026. Total revenue hit $22.2 billion, up 48% year-over-year. AI semiconductor revenue came in at $10.8 billion — a 143% year-over-year surge that beat the company’s own $10.7 billion forecast. Adjusted EBITDA reached $15.2 billion, representing 69% of revenue. Free cash flow hit a record high for the third consecutive quarter. Then the stock dropped 14% on June 4. In a market conditioned to expect beats and raises, standing pat reads as a warning. This is one of the most important patterns active traders must internalize about AVGO stock.

Q2 FY2026 Performance: Broadcom Inc. Financial Metrics

| Metric | Q2 FY2026 Actual | YoY Change | vs. Consensus |

|---|---|---|---|

| Total Revenue | $22.2 billion | +48% | Slight miss vs. $22.7B est. |

| AI Semiconductor Revenue | $10.8 billion | +143% | Beat ($10.7B forecast) |

| Non-AI Semiconductor Revenue | $4.2 billion | +6% | In line |

| Infrastructure Software Revenue | $7.2 billion | +9% | In line |

| Adjusted EBITDA | $15.2 billion | +52% | Beat (69% of revenue) |

| Non-GAAP EPS | $2.44 | — | Beat vs. $2.39 est. |

| Q3 AI Revenue Guidance | $16.0 billion | +200%+ YoY | Miss vs. $17.2B est. |

The reason was guidance. Broadcom projected Q3 AI semiconductor revenue of $16.0 billion — impressive by any historical standard, but $1.2 billion short of what analysts had modeled. The company also passed on raising its full-year AI outlook. The market reacted immediately. Broadcom shares fell approximately 14% on June 4, dragging the broader semiconductor sector lower with it. The number that matters is never what happened last quarter — it is whether management’s forward view matches what the market has already priced in.

The AI Revenue Engine: Two Tracks, One Story

Broadcom’s AI business runs on custom silicon and networking — and both are growing fast. On the silicon side, Broadcom designs ASICs tailored to each hyperscaler’s exact specifications. Google’s TPUs are the flagship example. These processors outperform general-purpose GPUs for specific AI tasks, and Broadcom’s multi-year design partnerships create revenue streams that competitors cannot easily disrupt. Management updates on TPU roadmaps and deployment timelines are among the highest-impact catalysts for AVGO stock. Networking represented nearly 40% of AI semiconductor revenue in Q2 FY2026 — a figure that continues to climb. That backlog provides demand visibility that stretches well beyond the current quarter.

On the networking side, Broadcom dominates the hardware that connects AI processors inside data centers. As model sizes grow and inference workloads expand, the demand for high-speed switching and routing hardware scales with them. Connecting thousands of AI accelerators inside a single data center requires Broadcom’s solutions at every layer of the stack. AI semiconductor bookings exceeded $30 billion in Q2 FY2026 — one of the strongest demand signals in the company’s history.

AI Revenue Breakdown: Accelerators and Networking Infrastructure

| AI Revenue Component | Q2 FY2026 Value | % of AI Revenue | Growth Driver |

|---|---|---|---|

| Custom AI Accelerators (ASICs) | ~$6.5 billion | ~60% | Google TPU, hyperscaler custom chips |

| AI Networking Hardware | ~$4.3 billion | ~40% | LLM scaling, data center connectivity |

| Total AI Semiconductor Revenue | $10.8 billion | 100% | +143% YoY |

| Q3 FY2026 AI Revenue Guidance | $16.0 billion | — | +200%+ YoY guided |

VMware: The Floor Beneath the Volatility

When chip markets turn, pure semiconductor stocks get hit hard. Broadcom stock absorbs that risk differently because of VMware. Infrastructure software revenue reached $7.2 billion in Q2 FY2026, up 9% year-over-year, representing 32% of total revenue. Recurring software income does not evaporate when AI spending slows — and that is precisely why it matters for traders and long-term investors alike. When money exits semiconductors, Broadcom does not fall as fast or as far as pure-play chip names. VMware’s margin profile adds compounding stability to an otherwise cyclical business.

The subscription transition is on track. Broadcom has successfully moved VMware customers from perpetual licenses to recurring subscription models, improving revenue predictability quarter over quarter. For active traders, this means AVGO stock has a meaningful earnings floor that cushions drawdowns during sector rotations. The combination of chip cyclicality and software stability is precisely what makes AVGO stock a differentiated holding in any AI-focused portfolio.

Geopolitical Risk: What the Strait of Hormuz Has to Do With AVGO

The June 4 selloff was not purely about guidance. Macro conditions made it worse. Iran’s Revolutionary Guard issued statements regarding the Strait of Hormuz in the same period, triggering risk-off moves across technology and energy-adjacent sectors. Broadcom sources components through Taiwan and Southeast Asian manufacturing networks — supply chains that sit directly in the path of the world’s most active geopolitical pressure points. These are not distant macro risks. They are operational risks with direct earnings implications. Improving trader skills in today’s market means understanding that semiconductor stocks do not trade on fundamentals alone.

A disruption in the Taiwan Strait tightens Broadcom’s supply chain immediately. Energy price spikes from Middle East tensions raise costs across its manufacturing partners. Tariff escalation between the US and China adds another layer of cost pressure on components that cross borders multiple times before reaching final assembly. Traders who build positions in AVGO stock without tracking these signals are missing a significant and recurring driver of short-term price movement.

What Traders Should Watch on AVGO Stock

Active traders need a clear framework for AVGO stock. The events below move this stock materially and repeatedly. Quarterly AI revenue versus consensus is the single most important number. Hyperscaler capital expenditure announcements are leading indicators for Broadcom’s ASIC order pipeline. Taiwan Strait and Middle East developments create volatility windows that experienced traders can position around.

Market Drivers: Key Catalysts for AVGO Equity Movement

| Trigger | Why It Matters | Typical Impact on AVGO Stock |

|---|---|---|

| Quarterly AI Revenue vs. Consensus | Guidance misses hit harder than beats reward | Sharp decline on miss; moderate gain on beat |

| Hyperscaler CapEx Announcements | Google, Microsoft, Meta, Amazon drive ASIC demand | Direct correlation to AVGO stock movement |

| Taiwan / Middle East Geopolitical Events | Supply chain and macro risk signals | Volatility spikes; risk-off selling pressure |

| Non-AI Semiconductor Bookings | Signals cyclical recovery in broader chip market | Upside potential beyond AI revenue alone |

| Full-Year AI Revenue Guidance Updates | Market demands progressive raises | Failure to raise triggers sell-the-news reactions |

Analyst Consensus and Price Targets

Twenty-six analysts cover AVGO stock. Not one recommends selling it. The consensus is Buy, with 42% at Strong Buy and 46% at Buy. At $385, AVGO stock trades approximately 27% below the median analyst target. The post-results pullback has reset valuation to levels that analysts view as a compelling entry point.

Broadcom (AVGO) Analyst Ratings and Market Sentiment

| Rating | % of Analysts | Price Target Range |

|---|---|---|

| Strong Buy | 42% | $450 – $550 |

| Buy | 46% | $420 – $520 |

| Hold | 12% | $350 – $420 |

| Sell | 0% | — |

| Median 12-Month Target | — | $490.00 |

| Current Price (June 7, 2026) | — | ~$385.00 |

| 52-Week Range | — | $241.11 – $495.00 |

Is AVGO Right for Active Traders and Investors?

Traders who do their homework on Broadcom’s catalysts and risk factors are operating with a genuine informational edge over those who simply react to headlines. Position sizing matters. Entry timing around earnings events matters. Understanding the guidance-versus-consensus dynamic is non-negotiable. This is not a stock you trade passively. The earnings pattern is well-established — strong results can still produce sharp declines when guidance disappoints. The geopolitical overlay adds another layer of complexity that separates informed traders from reactive ones.

For investors with a longer horizon, the picture is equally compelling. Broadcom pays a $0.65 quarterly dividend — something growth-only AI names do not offer. With 26 analysts and zero Sell ratings, institutional support for AVGO stock is as strong as it gets in this sector. A program for traders focused on risk-adjusted returns treats AVGO as a core position — significant exposure, carefully sized, never concentrated.

Best Stocks for Beginners: Where Does AVGO Fit?

Among the best stocks for beginners building AI exposure, AVGO stock offers a more forgiving profile than pure-play chip names. Three reasons stand out. First, the VMware software segment provides revenue stability that pure semiconductor companies cannot match. Second, Broadcom pays a $0.65 quarterly dividend — income that growth-only AI names do not offer. Third, with 26 analysts and zero Sell ratings, institutional support is as strong as it gets in this sector.

That said, a 14% single-day drop is not a beginner-friendly experience without preparation. Improving trader skills means understanding position sizing before entering volatile earnings setups. AVGO stock can be part of a beginner’s portfolio — but only with clear risk parameters and realistic expectations about short-term volatility.

The Q3 FY2026 Outlook

Broadcom guided Q3 FY2026 total revenue to $29.4 billion — 84% year-over-year growth. AI semiconductor revenue of $16.0 billion implies over 200% year-over-year growth. Non-GAAP operating margin holds at 67%, reflecting the operating leverage CEO Hock Tan has built systematically over the past decade. That tension is exactly what makes Broadcom stock one of the most compelling trading opportunities in the AI sector right now.

Q3 FY2026 Guidance: Broadcom vs. Analyst Consensus

| Metric | Broadcom Projection | Analyst Consensus | Gap |

|---|---|---|---|

| Total Revenue | $29.4 billion | ~$28.5 billion | Slight beat |

| AI Semiconductor Revenue | $16.0 billion | $17.2 billion | -$1.2 billion miss |

| Non-GAAP Operating Margin | 67% | ~67% | In line |

The central question for the next quarter is whether $16.0 billion in AI revenue satisfies a market that priced in $17.2 billion. If management delivers at or above guidance and signals an acceleration in the full-year outlook, AVGO stock could move sharply toward the $450-$490 analyst target range. If guidance underwhelms again, the stock faces another sell-the-news setup. Either way, Broadcom stock is not sitting still — and neither should the traders and investors watching it.

If you liked this post make sure to share it!